World

Why One Should Fear 2016: Rage In China, EU In A Mess, US Slowing, And India Clueless

V Anantha Nageswaran

Feb 16, 2016, 10:05 PM | Updated Feb 19, 2016, 03:53 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

The first few weeks of 2016 have been anything but quiet in the financial markets. There has been a lot of volatility and angst. Stock prices have tumbled in all major markets, including in the United States (though there has been some recovery in the Indian markets in response to the Bank of Japan’s decision to move towards negative interest rates, but this may not sustain). The price of crude oil has plunged below US$30 per barrel and anecdotal evidence suggests that maritime trade between North America and Europe was virtually non-existent in the first fortnight of January.

Those who think that what happens in financial markets concerns only the financial services industry should re-examine their assumptions. Writing in The Guardian, veteran journalist Will Hutton wanted a new generation of political leaders to throw off thinking in categories that have been cast since 1980. Since 1980, financial markets have figured prominently in the thinking among leaders. The three decades since 1980s featured not just the dominance of globalisation, the rise of China, outsourcing and offshoring of production but also saw an explosive growth in financial markets, in the development of new financial products and more importantly, in heavy borrowings both by governments and corporations.

Gross domestic product in advanced economies has gone up by around 5.6 times between 1980 and 2014. But, the amount of government debt in those countries has gone up nearly 15 times in the same period. This debt is like a rock placed on the shoulders of global economy. It cannot lift its back and walk, let alone sprint. The global economy will remain hobbled by debt, and economic growth will be a scarce commodity for a long time to come.

The economic and financial crisis in 2008 was a reminder of the fate that awaited us if the world persisted with its methods. Our policy leaders – politicians and technocrats – did not heed the message. Since 2008, they have been walking down the same path that brought peril to the world economy. Nearly seven years after the last recession in America was officially declared over, another one could be on its way in 2016. This time neither America nor the rest of the world has any tools left to deal with it.

The financial markets are not just about stocks and currencies. More than these two, the first signs of trouble have been evident in what are known as credit or bond markets. In December, at least three bond funds were distressed. Two shut shop and one refused to accept requests for redemptions since it was no longer sure of the value of the bonds it was holding in its portfolio.

Analysts with Standard & Poor’s, Moody’s and Fitch expect default rates to increase over the next 12 months, an inopportune time for Federal Reserve policymakers, who are expected to begin tightening of monetary policy in the coming weeks. S&P has cut its ratings on US bonds worth $1.04 trillion in the first 11 months of the year, a 72 percent jump from the entirety of 2014. In contrast, upgrades have fallen to less than $500 billion, more than a third below last year’s total. The rating agency has more than 300 US companies on review for downgrade, twice the number of groups its analysts have identified for potential upgrade.

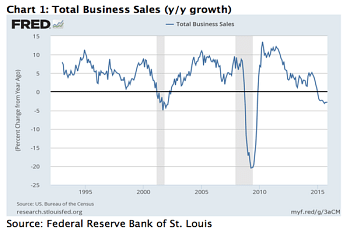

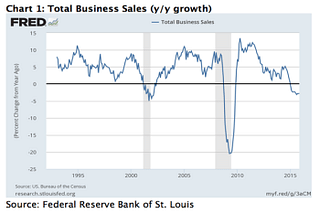

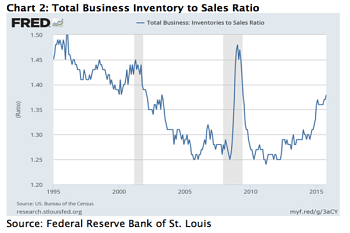

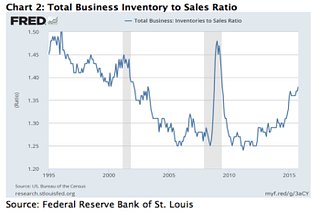

There are other reasons too to be worried about the outlook for the United States. Total business sales – the last data point available is for November 2015 – have been declining steadily in the course of 2015 (chart 1). The inventory to sales ratio is rising towards levels seen during recessions (chart 2) and the Index of Manufacturing is below 50. A recession in the US economy is a statistical possibility in 2016.

Chart 1: Total Business Sales (y/y growth)

Source: Federal Reserve Bank of St. Louis

Chart 2: Total Business Inventory to Sales Ratio

Source: Federal Reserve Bank of St. Louis

The Chicago Fed National Activity Index (CFNAI) is a comprehensive measure of national economic activity in the United States. The three-month moving average of CFNAI was at -0.20 in November. In recent months, the index has reflected the fraying of economic strength in the country. The index of optimism among small businesses compiled by the National Federation of Independent Businesses dropped to 94.8 in November. It peaked at 100.4 in December 2014. Now, it is almost back all the way to the levels that prevailed in 2010. This is what the Chief Economist of the NFIB had to say about the survey results for November 2015:

“In this “Season of Hope”, small business owners are finding little to be hopeful or optimistic about, including the economy in the New Year. Society is showing stress fractures all around, on college campuses, mass shootings, terrorist attacks, major cities and their police forces, scandals and incompetence rampant in DC, a Justice Department politicised, a political IRS and EPA running roughshod over individual rights and personal freedom, a Fed that can’t make up its mind about 0 interest rates “for too long”, a Congress that can’t seem to stay in the “power ring” with the President for a round, a President who thinks that our most important problem and threat is climate change (formally known as global warming) and is willing to punish the current economy for inconsequential benefits in the future just to set an example for the world (right!). It feels like we are starting to “lose it”, to dissemble.

“Well, the news isn’t all bad. The stock and bond markets are at record high levels. Unfortunately, that means the downside risk is huge! The dollar is strong and we are doing much better than most countries around the world. OK, that’s good, relatively speaking. The current NFIB survey reads are generally the best in this expansion, although historically below average in the 42-year history of expansions. The 1983-90 expansion created 689,000 jobs per quarter compared to 439,000 in this expansion, 2009 Q3 to the present – all that with a 30 percent smaller labour force back then.”[1]

However, there is some more time before problems in the American economy begin to dominate headlines. Before that, one has to deal with China.

The risk of the China rage

China’s economy has had a great run for nearly a generation. For the most part, it is still a successful story. But, only the passage of time will deliver a more impassioned and objective judgment. The costs of China’s miraculous transformation from an economy steeped in abject poverty to that of a middle-income nation are still being revealed, let alone being counted.

The costs, when they manifest fully, will not remain confined to China. There will be geopolitical and geo-economic costs. Globally, some are beginning to understand this while many remain in denial.

Much as China touted its own version of capitalism, it has not turned out to be dissimilar from the experience of other advanced economies. An explosive rise in debt, particularly since the advent of the new millennium, has played a big role in the rise of the Chinese economy. There is a reason why debt is called leverage. It can amplify both good and bad times. In the case of China, as much as the rest of the world, debt is showing its ugly side. The world is understandably nervous about China’s reaction as its government begins to realize that the economy can no longer be malleable. Economic growth has slowed in the country and the official growth numbers have justifiably become the butt of jokes. The government vainly tried to reduce the debt ratios in the economy by stoking an equity market bubble. That failed once in August.

The Chinese government pulled out a slew of unprecedented measures which made all activities in the stock market, except buying shares, illegal. That brought superficial stability to the state of affairs in Chinese markets and to global markets in the last months of the year. That illusion has been broken in the first two weeks of trading in 2016. China’s stock markets have cratered. All the gains that were engineered by government intervention since August 2015 have been erased. Chinese residents are seeking the safety of the US dollar. There is capital flight from the Chinese economy. The currency is weakening. China promised stability and a greater role for the market as it sought entry for its currency into the prestigious basket of currencies that constituted the currency of the International Monetary Fund – Special Drawing Rights (SDR). However, its domestic economic conditions leave no option for Chinese policymakers but to ‘borrow’ or ‘steal’ economic growth from the rest of the world through stealth or open currency depreciation.

Professor Zhiwu Chen, Professor of Finance at Yale School of Management, wrote:

“We can see why fundamental reforms are out of the question if we follow the quick logic chain: maintaining the party’s absolute control of economy/society is priority #1, far above and beyond everything else, for the current president —> SOEs (state-owned enterprises) must dominate economy —> banks and financial institutions must be controlled to serve the party and SOEs —> market principles must be restricted and capital in/out-flows cannot be free —> fundamental reforms continue to be talked about but not implemented, and structural imbalances cannot be corrected.

“If the SDR inclusion had happened three or four years ago, more real reforms would have been possible. But, right now, too many burning challenges and downturn pressures are at hand (e.g., overcapacity, capital outflow pressure, difficulty to achieve growth target even after many policy interventions, pollution and environment, all financing tools/channels exhausted to the limit and beyond). So, short-term goals are far more dominating, making the SDR story more of a transitory news event. Reality will be back soon.”

The world had adapted uneasily to the rise of China as a geopolitical and geo-economic force. But, now it has to learn to deal with the economic decline of China and the consequences that flow from it. Indeed, the big question is whether the rise of China would be replaced by the rage of China or, more precisely, the rising rage of China.

Even as Taiwan rejected the Kuomintang (KMT) party that favoured closer integration with the People’s Republic of China and elected the pro-independence Tsai Ing-wen of the Democratic Progressive Party as its next President in the elections held on 16 January, China made a teenage Taiwan singer submit a grovelling apology for waving the Taiwan flag at a performance. She was part of a Korean all-girl pop group.

The greater distance that the Taiwanese have preferred to put between themselves and the PRC should come as no surprise to those who have been watching international developments. In the last several years, China has systematically alienated almost all its neighbouring countries including Vietnam, the Philippines, Indonesia, Malaysia and, of course, Japan. Only the distant Europeans have been falling over each other in seeking China’s favour. Yet, China shows no signs of retracing its steps. It is calculating, or has miscalculated badly, that its time has come and that America has become politically effete. On 15 January, Financial Times reported that China had stepped up its construction of runways in the South China Sea since President Xi Jinping visited Washington in September, underscoring how US efforts to counter China’s assertive stance there appear to be having little effect.

The United States has not been passive, however. Contrary to popular expectations, it concluded a trade-promotion and trade liberalisation agreement with the nations that straddle the Pacific all the way from Chile to Vietnam. The Trans-Pacific Partnership (TPP) is awaiting approval from Congress. It has normalised relations with Vietnam and Cuba.

In December, it imposed duties of around 227 percent on imports of cold-rolled flat steel from China. It has removed economic sanctions on Iran and has even been prepared to isolate Saudi Arabia, its long-standing ally in the Persian Gulf. Perhaps, it quietly blessed the burial of the long-standing sore point – the abuse by wartime Japan of Korean ‘comfort women’ – between Japan and South Korea. Japan agreed to pay penalties for its conduct towards the women. All of these may have the effect of isolating China should there be an escalation in tensions with China over its economic policies or conduct in the South China Sea.

Consequently, the fear that should keep leaders around the world awake is the possibility that turmoil in the financial market will feed into and trigger an economic slowdown or even a meltdown. In its wake, geopolitical tensions and conflicts that have been simmering will boil over as nations look out for themselves rather than for each other. The collision of geopolitical, geo-financial and geo-economic tectonic plates is the biggest risk and possibility for 2016. ISIS looms large.

European social, political and economic tensions – from simmer to boil

The wounds inflicted on Europe by the Paris shootings in November 2015 will fester for a long time. It continues to divide Europe. Quietly, in the regional elections in France, voters gravitated towards the National Front that took a tough stance on foreign immigration into France. A ‘Fortress France’ mentality was taking over. The National Front’s inevitable march towards power has been temporarily delayed by an extraordinary round of coalition building and seat-sharing among major parties in the second round of elections.

Indeed, historical evidence is rather compelling that popular political preference shifts to the extreme-Right in the aftermath of economic crises. When economic crises are overlaid with civilisational clashes, the shift to the extreme Right is not only be more rapid but also last longer. Howard Davies, Chairman of the Royal Bank of Scotland, cites the original study for this conclusion in his piece published for ‘Project Syndicate’ on 22 December 2015.

Before the psychological wounds caused by the Paris shootings could become more bearable, came the news of the sexual outrage in Cologne, Germany during the New Year celebrations.

The European media has sought to deny the outrage or suppress the identity of the perpetrators for fear of stoking Islamophobia. But it is having the opposite effect. In the information-age, newspapers are not the only source of information. Hence, the vacuum left by the mainstream media is being filled by other sources both objectively and creatively. The only tangible outcome is the loss of credibility of the media and, if anything, stoking Islamophobia, the very outcome that ‘elites’ think they are avoiding, by their self-censorship.

In the US, a Muslim couple opened fire in San Bernardino killing fourteen people on 2 December 2015. The United States is now worried about the risks of human and other damage caused by the ‘lone wolf’ terrorist. Donald Trump, the front-runner the Republican candidate for the presidency, has called for a ban on Muslim immigration into the United States. This has provoked both condemnation and support. He is no fool to make these statements. He is tapping into the undercurrent of fears that are high among the public. Over the years, mainstream politicians and conventional politics have failed to deal with these fears and eliminate them. They have only grown. Demagogues have come up to fill the vacuum left by ineffective ‘moderates’.

Circling back to Europe, the tragic incidents in Paris and Cologne have not only exposed the fault lines in European societies generated by the influx of Muslims over the years, they have also badly damaged the political credibility and standing of Angela Merkel, the German chancellor.

In 2015, she had allowed about a million refugees from Syria to take up asylum in Germany. Her policy, even before these incidents happened, had attracted concern. Now, they are subject to severe opprobrium. She is politically damaged. She was a binding figure in European politics in the last two years as she played the balancing role between Southern European countries and her uncompromising cabinet colleagues. If she were to resign, it would reopen divisions within Europe. Towards the end of the year, in an interview with FT, the Prime Minister of Italy criticised Germany’s handling of European economic issues [4]. In Portugal, the European Commission tried to delay the assumption of office by a coalition of Left parties that had opposed the fiscal austerity imposed by the Commission.

The interplay of refugee and immigration politics and the social strains that they have unleashed come on top of the economic divisions and underperformance that continue to plague Europe. Germany has been the economic locomotive of the continent and the politically binding force in Europe. Its role in both these dimensions has become weaker. The scandal that engulfed Volkswagen has damaged German reputation for engineering excellence and integrity. It may have also undermined German export growth for 2016. Germany in recession with a politically damaged Chancellor could well be the catalyst for a fresh round of instability from Europe to be inflicted on a world grappling with a slowing and maverick China and an economically fragile United States.

Persian Gulf – the other geopolitical theatre

In the Persian Gulf, Saudi Arabia is increasingly feeling isolated. In the Global Climate talks in Paris, its stance was criticised. In the meeting of the Organisation of Petroleum Exporting Countries (OPEC) held on 4 December, its stance on not cutting production did not go down well with other members. Its patronage of a militant form of Islam is coming under intense scrutiny in the Western world as it executed a Shia cleric and cut off all trade and other ties with Iran, while engaging in a war of words with it.

In the meantime, Western economic sanctions on Iran were lifted around mid-January as scheduled. Iran’s oil exports look set to rise, further depressing the price of oil in the near term. At the same time, any small incident that shuts down the transit of oil from the Persian Gulf could send the price of crude oil shooting up by USD30-50 in a short time, further straining the economies of many developing nations. In other words, they appear doomed either way.

Crises have punctuated the march of prosperity

Many historians would say that the scenario of economic gloom and political doom is exaggerated. The world has lived through many crises in the past and prospered. Indeed, that is true. But, the world has also lurched from one crisis to the other during the modern era. Between 1885 and 1914, the world economy boomed. Then came World War I. Its end in 1919 heralded a boom in the US but not in Europe. Germany went into hyperinflation and saw the rise of Hitler. Then came the Great Depression. Its end was followed by a brief, shallow and uncertain recovery before World War II broke out. From 1945 to 1967, the world was busy with repair, recovery and reconstruction.

The war in Vietnam, the collapse of the Bretton Woods Exchange Rate regime, wars in West Asia, the rise of Opec, two oil price shocks and the Iranian hostage crisis punctuated the Seventies. The world began to recover – starting with the arrival of Reagan in the United States and Thatcher in Britain.

Then, the Soviet Union disintegrated and the Berlin Wall collapsed. Most of Western Europe came under a single currency. Globalisation and free trade became fashionable. So too did debt and finance. The world is again in trouble. Each spell of prosperity brings along with it excesses and mistakes that set up the next crisis followed by the next recovery. We are in the throes of one as the crisis of 2008 was not addressed but glossed over. Now, geopolitical overtones have complicated the task of handling the unfinished economic crisis of 2008.

India’s challenge

The challenge for India is immense. It has not yet recovered from the economic wounds inflicted by the previous government that was voted out of office in 2014. The new government finds itself overwhelmed by the challenges of reviving an economy that was left in a state of disrepair by the UPA government. Its biggest mistake was that it did not try to come to grips with the mess left behind. Before it could do so, the world economy changed and two bad monsoons had come and gone. India’s exports had contracted for the thirteenth month in succession in December.

Even though food prices contributed a great deal to the inflation outturn of 0.8 percent in December, that it amounts to an annualised 10 percent inflation rate amidst a stagnant economy says a lot about the inherent inefficiencies of the Indian economy.

The government has to grasp and accept that India is not in as sweet a spot as is being made out. It should desist being seduced by talk that India is the world’s fastest growing big economy. It is nowhere near that. The economy is stagnant. The farming sector is weak. Banks are undercapitalised. Spirits are reviving only hesitantly, if at all, in the private sector. The anaemic state of the world economy is such that global markets are effectively shut for India’s exports. The dismal state of productivity of Indian manufacturing compounds the export growth problem. In the meantime, a weak Chinese currency threatens to pull the rug from under the feet of India’s exports completely.

It requires realisation (an acceptance of the economic and geopolitical reality); communication (to be in touch with the public and to show that one has not lost touch with the reality); and imagination (to realise that the time for incrementalism is long past) on the part of Indian leadership to guide the country through what are likely to be treacherous times. Otherwise, as the world steps on to economic and political landmines in 2016, some of them would explode in India’s face too.

References on next page

[1] See http://www.nfib.com/surveys/small-business-economic-trends/

[2] See

[3] See https://www.project-syndicate.org/commentary/financial-crises-political-consequences-by-howard-davies-2015-12

[4] See http://www.ft.com/intl/cms/s/0/c6ab59e2-a8c1-11e5-955c-1e1d6de94879.html

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

V. Anantha Nageswaran has jointly authored, ‘Can India grow?’ and ‘The Rise of Finance:Causes, Consequences and Cures’

Introducing ElectionsHQ + 50 Ground Reports Project

The 2024 elections might seem easy to guess, but there are some important questions that shouldn't be missed.

Do freebies still sway voters? Do people prioritise infrastructure when voting? How will Punjab vote?

The answers to these questions provide great insights into where we, as a country, are headed in the years to come.

Swarajya is starting a project with an aim to do 50 solid ground stories and a smart commentary service on WhatsApp, a one-of-a-kind. We'd love your support during this election season.

Click below to contribute.