Economy

Explained: The Comprehensive And Sector-Specific Guidelines Given By Kamath Committee For Loan Restructuring

Karan Bhasin

Sep 10, 2020, 02:45 PM | Updated 02:44 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Recently, the K V Kamath committee report was made public by the Reserve Bank of India (RBI). The committee was formed to improve the transparency of the loan restructuring process that Indian banking system will have to undertake over the coming months.

There are three specific issues that need to be understood in order to appreciate the need to allow for restructuring of loans.

In the present scenario, when we have witnessed a prolonged lockdown in several parts of the economy, several companies may invariably default on their previous borrowings which could result in an increase in non-performing assets (NPAs) for banks.

India’s banking sector has barely managed to heal from the previous NPA mess and this could create fresh troubles for their balance-sheet.

Consequently, higher NPAs mean higher provisions for losses by these banks and thus, they would be reluctant to lend which will only worsen the economic situation.

By allowing banks to restructure loans – that is, change in the rate of interest, repayment terms and other provisions – there is a possibility to prevent massive bankruptcies and avoid another NPA fiasco.

Even with the one-time restructuring, we will witness 8-10 per cent of NPAs. Yet, this is important as it will give banks an opportunity to prevent an unprecedented level of wealth destruction.

The reason behind setting guidelines was to avoid discretion at the hand of bankers – which could lead to corruption, collusion and prospects of misuse of the provision as it happened during the UPA period.

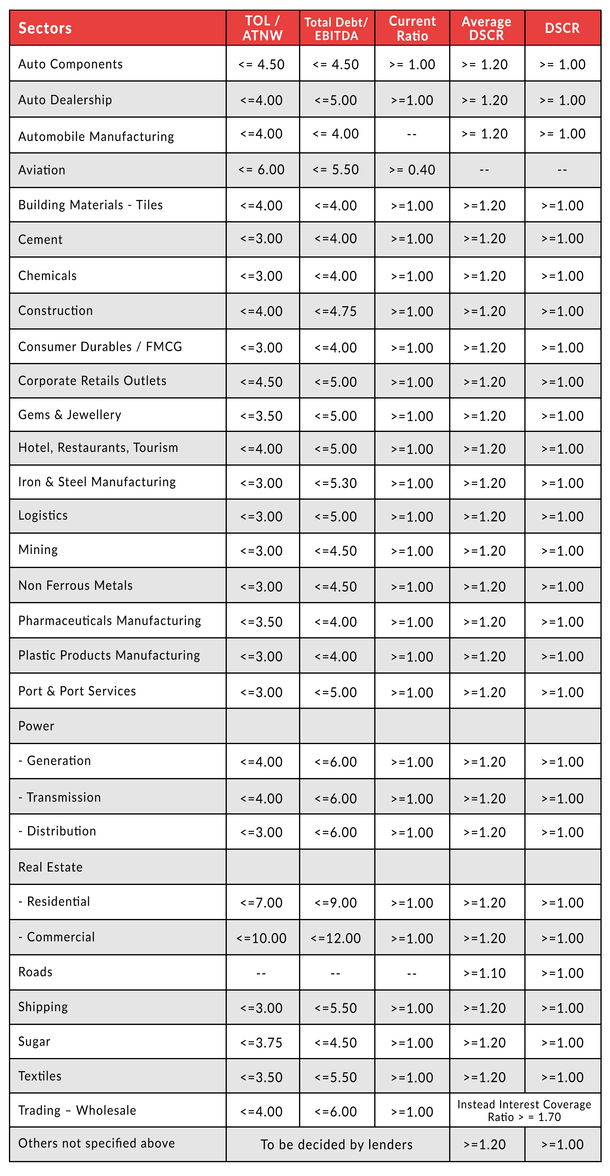

Consequently, the report has gone into granular details by considering the following criteria for restructuring and prescribing the ratios for each individual sector (enclosed in Table 1).

- Total outside liabilities/adjusted tangible net worth: This ratio is of the existing outside liabilities of a company and the net worth of a company. It essentially gives an idea of how much liability a company has in contrast with the tangible net worth of the company.

- Total debt/EBITDA: This measures the ratio of the total borrowings of the company as against earnings of the company before interest, tax, depreciation and amortisation.

- Current ratio: Current ratio is a measure of liquidity ratio. That is, it measures a company's ability to pay short-term obligations or those due within one year.

- Debt service coverage ratio: The debt service coverage is the ratio of operating income available to debt servicing for interest, principal and lease payments. It measures the ability of a company to generate adequate income to meet its debt obligations.

- Average debt service coverage ratio.

For all other sectors, the committee has left it open to the lenders to determine the terms of the restructuring.

However, there are a few interesting observations that must be made. Sectors such as real estate, aviation, automobile, hotels and corporate retail have been given the highest ratios.

That is, for a company with total outside liabilities divided by the adjusted net worth equal to (or lower than) 10 for commercial real estate, banks are allowed to restructure the loan, while the same for aviation is 6.

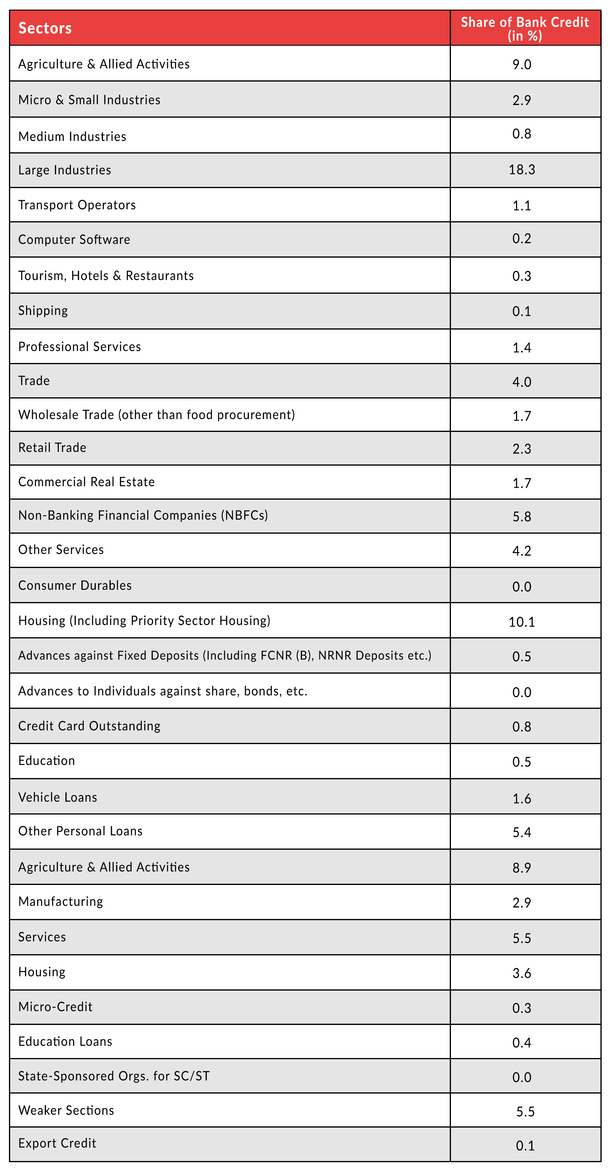

It is interesting to note that these new ratios are also in line with the share of bank credit distributed across different sectors and suggest that the government is looking to limit the extent of NPAs (refer to Table 2).

The distinction between these ratios is a welcome measure and shows the comprehensive understanding of our banks, and the central banker regarding the differential impact of the pandemic on sectors.

This is precisely why sectors such as corporate real estate, automobile production, aviation and tourism have allowed for a higher limit for restructuring – potentially with the intention of covering as many companies as possible.

The other good aspect is the extent of granular detail which while leaving some flexibility creates a more rules-based system for restructuring. This will likely prevent this exercise to allow for inefficient capital allocation in the economy.

On the flipside, there are concerns regarding the ratios becoming too rigid that they end up in companies fudging numbers to become eligible for restructuring of their debt. This has been a concern as across the world several such instances have occurred and this makes due diligence all the more essential.

Ultimately, what happens to the balance-sheet of banks would depend on a host of factors and we may end up requiring recapitalisation of the banks to tide over the financial stress caused by the pandemic.

However, the report and measures taken have been proactive in limiting the extent of the damage to the financial sector. All eyes are now on India’s banks – and their ability to come through and contribute their bit in combating one of the biggest economic challenges India has faced in history.

Get Swarajya in your inbox.

Magazine