Economy

How Real-Time Data Exchange Can Help Solve The Multiple Loans Problem

Mani Parthasarathy

Jul 19, 2024, 12:53 PM | Updated 02:28 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

.jpg?w=610&q=75&compress=true&format=auto)

.jpg?w=310&q=75&compress=true&format=auto)

The Reserve Bank of India (RBI) has been issuing warnings to banks and non-banking financial companies (NBFCs) about the high growth in personal loans, algorithmic credit score-based unsecured lending, and so on consistently in the last few months.

While the overall health of the banking system is in excellent condition with historically low non-performing assets (NPAs) and healthy profitability, very high growth in unsecured personal loans is one area that causes some concern.

Readers may recall that it is this segment of loans that was the trigger behind the big global financial crisis in 2007-08, one of the most severe worldwide economic crises since the Great Depression.

In the banking and lending sector, taking out multiple loans for a single enquiry presents a significant challenge, often leading to substantial financial losses for both institutions and individuals.

A common issue arises when agents persuade customers to apply for loans from multiple lenders at once, exploiting the lack of communication between these institutions to secure more credit than the customers are eligible for.

Let's delve into this problem and explore a solution that harnesses the potential of real-time data exchange.

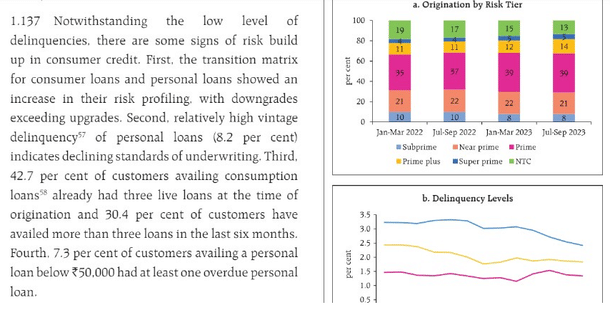

According to data from the RBI, a staggering 42.7 per cent of customers who have taken a consumer loan already had three live loans at the time of loan origination. This data point indicates a concerning trend of overborrowing among consumers, potentially increasing the risk of default.

Understanding The Problem

Consider this scenario: Mani applies for a personal loan of Rs 100,000 on Day 1, and his document is shared by the channel partner with Bank A and Bank B concurrently.

Surprisingly, both banks approve the loan, unaware of the other's decision.

Consequently, Mani ends up with a total loan amount of Rs 200,000, potentially exceeding his eligibility.

This situation highlights a critical flaw in the lending process. Without a mechanism for sharing information about loan applications and approvals across institutions, lenders operate in silos, leaving room for exploitation by fraudulent individuals.

The Solution: Leveraging Real-Time Data Exchange

To address this challenge, organisations like the Credit Information Bureau (India) Limited (CIBIL) have introduced innovative solutions. One such solution is the implementation of an alert system that facilitates daily (real-time) updates on loan enquiries and disbursals.

Here's how it works:

Real-time data submission:

Banks and financial institutions are encouraged to submit information regarding loan enquiries and disbursals to CIBIL on a daily basis (real-time). This includes details such as the applicant's name, loan amount, enquiry date, and disbursal status.

Centralised monitoring:

Credit information companies (CICs), such as Transunion CIBIL or CRIF Highmark, serve as a central repository for this data. By maintaining a comprehensive record of loan activities, CICs enable lenders to access real-time information about an individual's borrowing history.

Prevention of multiple loans in a single enquiry:

Returning to Mani's case, when Bank A disburses the loan on Day 1, it promptly updates this information with the CICs. Consequently, when Bank B processes Mani's loan application on Day 2, it can cross-reference CICs’ database. Upon discovering that Mani has already received a loan from Bank A, Bank B can prevent further disbursal, thereby thwarting potential fraud.

While the concept of real-time data exchange holds immense promise, its implementation requires robust infrastructure and technological capabilities. Several new-age NBFCs, financial software vendors, and so on are coming up with such features to implement this solution.

However, a regulatory guidance towards this move would provide the necessary fillip for the banks to adopt the same, in their own interest of the health of their personal lending portfolio.

In the fight against fraudulent activities in lending, real-time data exchange emerges as a powerful ally. By fostering transparency and collaboration among financial institutions, technological solutions have the potential to revolutionise the lending landscape.

As we embrace the era of digital innovation, leveraging technology to safeguard the integrity of financial systems becomes imperative. Through collective efforts and innovative solutions, we can build a more secure and resilient lending ecosystem for the benefit of all stakeholders.

Mani Parthasarathy is CEO, CloudBankin.

Get Swarajya in your inbox.

Magazine