Economy

One Month Into Demonetisation, These Are The Issues That Are Now Being Discussed

V Anantha Nageswaran

Dec 15, 2016, 09:20 PM | Updated 09:20 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

It is almost five weeks since the Indian Prime Minister announced his great monetary policy experiment. He already has a follower. Venezuela announced one recently. Not that the country (Venezuela) is a disciple that PM Modi can proudly show off! Many commentators are unwilling to wait. They want a judgement here and now – positive or negative. Reality is seldom that neat, if ever.

RBI has announced that the Specified Bank Notes of Rupees 500 and 1000 denomination (SBN) returned to its chest amounted to INR12.44 trillion. SBN as of March 2016 was INR14.18 trillion constituting 86.4 per cent of total currency in circulation. I do not know if anyone has information on the amount of SBN in circulation as of November 7 or 8, before the announcement. If not, then 87.8 per cent of the SBN in circulation has already been returned to RBI. That is staggering.

As someone wrote, perhaps, the government has underestimated the Indians’ ability to launder money. It is not a joke. It is a severe indictment of the country actually raising profound questions on its future prospects.

Few days ago, I stumbled upon posts on India’s currency swap by Raghav Bahl who started TV 18 and has now set up Quint media. I also read other pieces of him, unrelated to demonetisation. Overall, one should be careful not to be swayed too much by the colourful graphics and dramatisation. Substance is on the shallower side. In fact, in some cases, they are wrong. You can see his pieces here, here and here.

There are some unnecessary and culturally loaded references to people ‘eating greasy vegetarian meals’ and sitting down to listen to the Prime Minister’s speech on November 8. He does not seem to understand (or, deliberately conflates) that not all deposits into the banking system would leave. It depends on how much of ‘transactional’ cash and ‘store of wealth’ cash were deposited.

Yes, I understand the argument. The public deposits cash because they have been told to do so. Only then, can they get new notes. So, as soon as new notes are available, they would withdraw. Some deposits are stuck there now because new currency notes are not available. As soon as they are available, these deposits would be withdrawn. But, most of these conceptual issues have to have orders of magnitude attached to them to be taken to the next level of discussion. Otherwise, in business-school lingo, it is ‘class participation’.

On a side note, it was amusing to note several prominent media personalities tweeting his articles as their contribution to the rigorous analysis of the government’s action.

He had a piece on Raghuram Rajan’s departure. In that piece, he betrayed his lack of understanding of the concepts of inflation targeting and nominal GDP targeting. There is no difference. The latter is a more egregious form of the former. It is cumulative inflation targeting!

Good friend TCA Srinivasa Raghavan sent this article. Very interesting. Did not know that the British government ordered a ‘note bandi’ in 1946. It did not go down well nor does it appear to have succeeded.

The article by Srinath Raghavan in Hindustan Times on the Gold Control decision of Shri. Morarji Desai, Finance Minister in Jawaharlal Nehru’s cabinet is equally instructive. People find ways to get around seemingly draconian orders. Is that a good thing or bad thing? We do not know. Both, perhaps. [If one wanted to read the history of various episodes of demonetisation, one can and should bookmark a widely followed blog, ‘Mostly Economics’. Amol Agrawal is a prolific blogger – more prolific than Yours truly. Mine is episodic]. Back to Srinath Raghavan.

His article in MINT equating the government’s ‘currency swap’ with central planning is a shocker. What the government has done is not central planning at all. One can call the government’s decision by any other (worst) name, if one did not like it. But, ‘central planning’, it is not. It makes one feel sad to see people one holds in high regard succumb to passion and sacrifice perspective, in the process.

Praveen Chakravarty is somewhat angrier too here but less so than Srinath Raghavan. He suggests that shifting the goalposts of the ‘currency swap’ exercise from corruption, black money and terrorism to ‘less cash’ or ‘cashless’ is not only wrong but casual and careless. He contrasts the persuasive ‘Swachh Bharat’ exercise with the coercive strike on black money. In his view, the latter goals do not warrant imposing such enormous (in his view) hardship on the people. He calls it primordial. Interesting arguments and not entirely unreasonable.

But, political rhetoric can shift. That is par for the course for politicians. Corruption, black money and terrorism remain the principal goals. That was the policy announcement. Going ‘less cash’ or ‘digital’ are also instruments against future generation of corruption, black money and persistent informalisation. To harp on it over and over again might scare the public. Therefore, taking it as one’s point of analysis is a bit harsh.

That brings me to another point. There is a lot of confusion and misunderstanding about what constitutes informal sector. But, the confusion is widely shared and even international. There is a political correctness in not equating it with black economy. But, regardless of how one views the sector on humanitarian grounds, it is black economy, unreported, untaxed, unregulated and underground. It is a subset of the black economy.

Professor Freidrich Schneider’s taxonomy of the informal sector is useful:

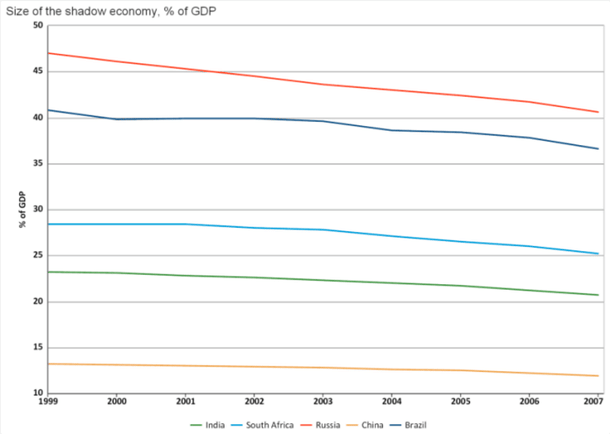

Professor Freidrich Schneider at the Johannes Kepler University of Linz has been one of the foremost researchers on the ‘Shadow’ or Informal Economy. His paper, ‘Shadow Economies and Corruption All Over the World: What Do We Really Know?’ published in September 2006 is a very useful and comprehensive reference. It provides international comparisons. In this paper, he puts the estimate of the shadow economy in India at 25.6 per cent as of 2002-03.

However, there is an updated paper (July 2010) in which he is a co-author and in that paper, the estimate is 20.7 per cent as of 2007. Even the figure of 25.6 per cent for 2002-03 has been revised down to little over 22 per cent.

With Knoema.com, you can chart it. Apparently, the site combines the word, ‘Knowledge’ and the Greek word, ‘noema’, which stands for “what makes sense”. For what it is worth, find below the chart for the size of the shadow economy in BRICS countries with data from Knoema.com.

With the International Labour Organisation putting India’s informal employment at 83.6 per cent, my guess is that both estimates (25.6 per cent and 20.7 per cent) are somewhat on the lower side.

Interesting that this World Bank Viewpoint Note on the informal sector in Brazil makes the point that informal enterprises do not join the formal sector on their own:

Informality impedes private sector development by undermining investment and productivity growth. Contrary to what many people have argued, informal firms do not always “grow up” and join the formal sector. Instead, they can remain stuck in an informality trap, excluded from markets for finance and forced to evade taxes and other regulations to compete with their more productive rivals. The solution lies in a mix of stronger incentives for compliance and stiffer penalties for noncompliance. [Link]

I examine the issues related to the informal sector in my recent MINT column. I cite the articles written by Niranjan Rajadhyaksha and Manas Chakravarty both of whom deal with the informal sector in different ways. Alex Tabarrok’s points that Niranjan helpfully cites in his piece are rather critical:

India’s dilemma is that its high productivity sectors are taxed while its low-productivity sectors aren’t, so valuable resources are trapped in low productivity sectors. Modi knows this and if he is serious then his surprise demonetization will be followed by more efforts to bring India’s informal sector into the formal sector, leveling the playing field, and increasing total wealth. [Link]

The question is what does the government have in store – the bag of tricks of incentives and disincentives. There, we do not have much to go by. Yes, there are concessions for digital transactions and hints of tax cuts. But, what we need is a thought process and a draft action paper on the informal sector. That is missing. Please correct me if I am wrong.

What we have is a series of T.V. interviews by Mr. Gurumurthy – who does not have any formal role in the government. However, interestingly, Gurumurthy had flagged his own role and the government’s intentions way back in June when he wrote after Raghuram Rajan announced his decision in June to leave the Reserve Bank of India in September:

With the credit offtake falling in a rising economy, the RBI ought to be clearly seeing where the vitamin of money comes from to finance the higher growth. The new finance is sourced in an unprecedented rise in cash holdings which have risen to Rs 15 lakh crore in 2015-16 with the share of high denomination notes in the total currency in circulation rising from 33 per cent to 85 per cent in 2015-16. These distortions were occurring under the very nose of Rajan. But he overlooked them, because he had never handled economies where banks do not control the entire monetary system. [Link]

n one of those interviews, he talks of the ‘Manmohan Singh model’ (yes!) of providing financing to small and medium enterprises (SME).

Apparently, back in 1993, the then Finance Minister Manmohan Singh allowed refinancing of non-banking financial corporations that made loans for purchase of second hand and third hand commercial vehicles. Mr. Gurumurthy argues that it created a boom in that sector and he wants it replicated for the entire SME sector, through the ‘bounty’ that the government and the banking sector would collect, once the exercise of ‘currency swap’ ends officially on December 30.

He attributes the rise of the proportion of the cash economy to GDP and the rise of proportion of High Denomination Notes (HDN in the overall cash) to asset inflation (bubbles) led growth in the UPA years and financialisation of the Indian economy.

I found the following information on the proportion of HDN in the overall currency in circulation in the economy from RBI Annual Reports: It stood at 26.7% in March 2001. It rose sharply to 47.0% by March 2004, had jumped to 73.5% in 2009 and to 84.0% in 2014.

For evidence (of the role of asset prices in propelling economic growth), he cites the lack of overall jobs growth in the Indian economy in the UPA (I and II) years. Data for the UPA II is only partially available. It is two years since UPA was voted out of office! That is Indian statistics for us.

As per Labour Department Statistics, during the NDA 1 years (1998-2004), there was overall employment growth (around 60 million) but not in the organised sector. In the UPA years, it was the other way around. In fact, excluding the construction sector, there was net job loss during UPA years up to 2010. But, there was jobs growth in the organised sector. Indeed, Mr. Gurumurthy would argue that it proves his point. That the fruits of asset prices-led economic growth during that period was only available to select few in the country.

As for how the cash found its way into asset markets, he calls it a quadrangular relationship between cash, gold, real estate and stock markets that reinforced each other. He is making plausible arguments and these are interesting hypotheses. Not without merit, either.

Many of us had written in 2006-08 period that India’s economic growth in that period was unsustainable and of low quality. I can immediately think of myself and my friend Niranjan Rajadhyaksha in MINT. Even this hyped-up economic growth paled in comparison to how well Indian stocks did. As a representative evidence, one can point to the fact that the Mumbai Sensex index shot up from 2600 points late in 2002 to around 21,000 points early in 2008.

Some would argue that this was fuelled by the inflow of capital from foreign institutional investors. Those come through banking channels. True, at first glance. But, there is a rider. The role of Participatory Notes has to be taken into account. These are instruments supposedly meant to allow non-resident individual investors to hold on to the coat tails of Foreign Portfolio Investors to invest in Indian stocks. In reality, many argue that Indian residents used it to launder money overseas and participate in Indian stocks with the benefit of repatriation into a foreign currency and without paying taxes either, since these monies were routed through jurisdictions that had tax treaties with India. Very neat. It was the ‘Great Gatsby’ era for many economies around the world and India was very much in the thick of it.

The orders of magnitude were substantial:

As things stand, P-Notes make up around 15-20% of the total FII investment in India since 2009. While it used to be much higher, 25-40% in 2008, the reading was as high as over 50% at the peak of stock market bull run in 2007. [Link]

Dr. Y.V. Reddy, former Governor of the Reserve Bank of India was categorical in his assertion of the pernicious role of participatory notes in fuelling black money. Listen to his speech in Bhopal delivered on October 5, 2016 (my date of birth!).

[Interestingly, a website named gfintegrity.org (Global Financial Integrity) puts the annual average illicit financial outflow from India in the decade from 2004 to 2013 at USD51bn. It is USD140bn for China, USD105bn for Russia, USD23.0bn for Brazil and USD21.0bn for South Africa.]

So, his solution is to bring this cash that was merely fuelling asset prices and creating a facade of economic growth without creating jobs into the formal economy through this sudden, one-shot, secretive currency swap move. He thinks that there was no other way it could have been done and waiting for a few more years would have made the situation irretrievable.

Of course, some disagree. Madhav Dhar, a fund manager lists the following prerequisites before undertaking the surgical strike on cash:

The objective is very noble, so was Gareebi hatao. Who can argue against that? Who can argue against elimination of black money? But how you go about it, what pre-conditions you out in place, what behavioural changes you seek so it doesn’t happen, those are the planks you have to put in place before the fact, and that that certainly hasn’t happened. So before you really put India in a different path altogether, both sociologically and economically, you would have said everybody has to get an Aadhaar card. When they get an Aadhaar card, they get an automatic bank account, then they get a debit card whether they like it or not. So that has to be the sequence. Then you say how political parties are going to get funded has to become transparent. Then you make it clear that tax laws are such that are three or four slabs with minimum changes and minimum deductions. And then you say, after all, that we will give you six months to get out of cash otherwise we are going to come down very hard on you. That’s the way to do it. [Link]

It sounds nice and logical. But, well, does ‘stuff’ happen in India without crises? If you asked Shankkar Aiyar whose ‘Accidental India’ was one of my most favourite reads of 2016, the answer would be an emphatic NO. So, has the government engineered a crisis to leapfrog the Indian economy and crash through (or, rush through) some of the things that needed to be done but would have otherwise taken eons to happen? An interesting thought but difficult to establish one way or the other. In any case, the evidence won’t be in for a few years. That has been my refrain in any case in the last one month. This policy decision cannot be objectively evaluated in real time. That does not mean evaluation won’t happen, however.

Back to Gurumurthy. His proposal is to use the cash collected through the surgical strike – well prepared move or not – to distribute it to the poor through cash transfers and by offering credit to the SME through the banking system. Hence, his reference to the ‘Manmohan Singh’ model of 1993.

These are, prima facie, good and interesting proposals. But, they need to be subject to a much wider debate. That is crucial. Individually, many of these arguments make sense but whether they do so collectively remains to be established. Further, distribution of cash and provision of credit may constitute only a partial set of necessary conditions and certainly not sufficient conditions for formalisation of the economy and further sustained and sustainable economic growth. Will have more to say on it in the weeks ahead.

Rajrishi Singhal makes a thoughtful point that the law of unintended consequence could operate with respect confidence in the banking sector. If the public deposits money into banks and is unable to withdraw it or if the bank denies it (even if only for a short period), then, it can lead to the public losing confidence in banks. I agree. That risk exists and it is not trivial, if the notes shortage in banks persists.

An unusually angry Andy Mukherjee echoes him on the unintended consequences on the banking sector here:

Amid the chaos, discussions about improving the governance of India’s dominant state-run banks, and selling or shuttering the weakest of them, have come to a standstill. The more urgent task of cleaning up their compromised balance sheets has also lost the steam it had gathered under previous RBI Governor Raghuram Rajan. If a month ago there was fond but foolish hope that banks would get a big one-time recapitalization boost, now there’s despair about how long they can go on fighting fires without any chance of a revival in credit demand.

It’s hard to believe Prime Minister Narendra Modi didn’t think through these unintended consequences. [Link]

Read this one too where he argues that RBI should have cut rates. But, nothing prevents the banks from cutting their lending rates, if they have cut their deposit rates.

The government’s lack of preparation could have been and should have been discussed by making it prepare well at least to answer questions on its lack of preparation. The Opposition has failed to do that. It was an opportunity lost for them and for the government to share its thinking more transparently with the Opposition and with the public. Shankkar Aiyar, as thoughtful as ever, makes these points here.

Prof. Ken Rogoff also thinks that the government has bitten off more than what it could chew. He is still positive about the move despite its ‘drastic’ nature.

In an economy profoundly crippled by tax evasion and corruption, India’s radical demonetisation may yet have positive long-run effects. In a sense, Mr Modi’s broader goal is to change the mindset of India.

The FT header sounds a little bit too critical than his piece itself.

It has been a long post in the making. Time to wind up. I shall do so with a link to a recent column by R. Gopalan (former Secretary of the Department of Economic Affairs, Ministry of Finance, Government of India) and his co-author on the economic growth impact of the currency swap. They argue, echoing the notes I had seen from Neelkanth Mishra (and his team) at Credit Suisse, that GDP growth statistics for the fiscal third quarter (October – December 2016) and fourth quarter (January – March 2017), counting as they do the visible sector, could understate the true negative impact on the real economy since much of it is borne by the cash-based informal sector. Gopalan and his co-author argue that it could last 3 to 4 quarters.

I noticed that I had called comments by three respectable and thoughtful commentators as angry. That is something for the Prime Minister and his office to think about. If the law of unintended consequences combined with bad planning makes collateral damage the central (and persistent) story of currency swap, (heavy and likely adverse) political consequences would follow. Oh, well. There will be other occasions to dwell on the consequent unpleasant prospect for the Indian economy.

This piece was first published on The Gold Standard and has been republished here with permission.

V. Anantha Nageswaran has jointly authored, ‘Can India grow?’ and ‘The Rise of Finance:Causes, Consequences and Cures’

Get Swarajya in your inbox.

Magazine