Business

Telecom Sector Is In Poor Health, But Here’s How It Can Recover

Swati Kamal

May 19, 2018, 01:17 PM | Updated 01:17 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

The health of the telecom industry appears conclusively to be in the red zone. Vodafone India recently announced its fourth quarter 2017-18 results – as against a revenue of Rs 10,547 crore in the fourth quarter of 2016-17, this year’s revenue was Rs 7,902 crore – a 29 per cent drop.

Earlier, it was Airtel’s India operations that reported their first loss in 15 years – Rs 652 crore – in the fourth quarter of fiscal year 2018. Idea’s losses were reported to be Rs 4,141 crore recently.

Jio to blame?

Widely, Reliance Jio is being blamed for the state of affairs in the telecom sector. Even the Economic Survey 2017-18 had said: “It is important to note that the telecom sector is going through a stress period with growing losses, debt pile, price war, reduced revenue and irrational spectrum costs. A new entrant has disrupted the market with low-cost data services and the revenue of incumbent players has fallen. The crisis has also severely impacted investors, lenders, partners and vendors of these telecom companies.”

Last year’s Economic Survey (2016-17) had said something similar. “The telecommunications sector has experienced its own version of the ‘renewables shock’ in the form of a new entrant that has dramatically reduced prices for, and increased access to, data, thereby benefitting—at least in the short run— consumers. But.. the near term implications for the viability of incumbents are serious...”

The Survey reported that the profitability of the incumbents had fallen “dramatically”, adding, “not only is the banking system exposed but so too is the government to whom the companies owe a variety of fees and taxes.”

Poor health of the industry is historic

The Reserve Bank of India’s Financial Stability Report, December 2016, had listed telecom among the three most indebted sectors along with iron and steel, and power. Significantly, Jio made an entry after this development.

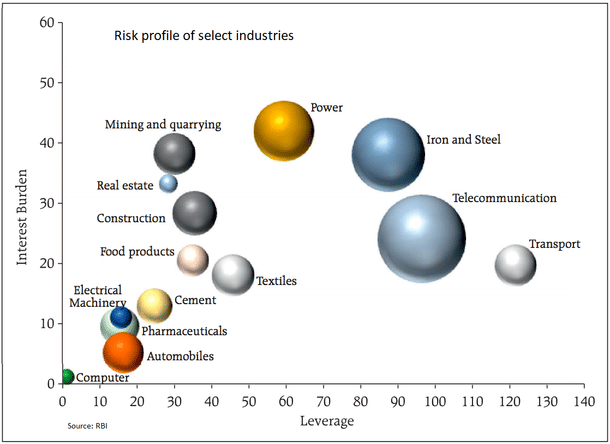

The chart in the report is reproduced below, depicting risk profiles of industries as on September 2016. Note that telecom is the biggest bubble. The accumulated debt of telecom companies, or telcos, was already Rs 3.8 lakh crore, according to a report by industry body the Associated Chambers of Commerce and Industry of India (ASSOCHAM) and consulting firm KPMG. The interest-coverage ratio for the sector stood at less than one. (Interest coverage ratio is an indicator measuring the debt-servicing ability of the borrower; a ratio of less than one indicates a company’s inability to honour payments). High debt levels also increase interest costs and impact debt servicing.

High debts in telecom are a universal phenomenon

Telecom needs large investments in infrastructure and networks, and thus ends up being a capital-intensive industry. ‘The Debt Report: the Telecom Sector in 2016’ talked about how debt was piling on for telecom providers in the United States (US), with the debt-to-assets ratio at 45-48 per cent on an average. Sprint Corp, for instance, even reported negative cash flows, making prospects for repayment bleak. And though competition has been pushing capital expenditures (CAPEX) higher, profits are falling. Operators are struggling with competition, and data services have eaten into voice and short message service (SMS) revenues. On top of all this, telecom frauds are increasing and affecting revenues of operators.

Consolidation is the flavour of this era – just last month, US wireless companies T-Mobile US Inc and Sprint Corp merged. The latter had been saddled by huge debt, and this combined entity now hopes to forcefully compete with AT&T and Verizon, both of who are also in the process of acquisition across sectors – like AT&T trying to acquire media giant Time Warner.

In the Indian context, Reliance Jio went ahead and did exactly what had been the norm across the world for years – increasing data availability, investing in long-term evolution (LTE)-enabled technology, buying over media networks and working towards supplying content, integrating it with other anticipated needs of the economy, and so on; in other words, provision of integrated telecom services. The other telcos lost out owing to their outmoded thinking, reliance on voice for revenues, and not investing in services – in other words, merely playing the role of giver of phone connections.

Way ahead for the industry and government

Deloitte in its 2018 ‘Telecommunications Industry Outlook’ especially emphasises that because revenue yield on data services continues to decline as consumers use more and more data, it is “critical to identify rapid investment opportunities across the telecom portfolio—including 5G, IoT (Internet of Things), and cross-industry partnerships (such as mHealth and mPayments), as well as a host of other growth opportunities”. Connected cars and other things like home maintenance, wearables, workforce training, entertainment – the sky appears to be the limit as far as IoT goes. Telecom carriers across the world are looking at partnerships with mobile content, infotainment, telemedicine, and so on for achieving growth. And mergers and acquisition, and consolidation are the order of the day, including in towers and network. Logically, this is the way Indian telcos need to look, and indeed, they are waking up to it – even if Jio showed the way.

Government’s role requirements

For decades now, there have been demands for rationalisation of various duties, fees, spectrum charges, and taxes by industry, as well as recommendations for the same by organisations with stakes in the sector, that is, Telecom Regulatory Authority of India, Ernst & Young, KPMG, and others. Former State Bank of India chairman Arundhati Bhattacharya had voiced her concerns about the “unsustainable levels of debt” and asked for a bailout package comprising duty waivers, deferred spectrum payments, lower goods and services tax, and so on, to save the “bleeding telecom companies”. In all likelihood, the government will do all it can – because of its keenness to move to Digital India and the critical nature of the industry to the Indian economy. In the US, the government reserves spectrum for the smaller players currently; only the big players with deep pockets now survive in India. But at a later point, this could be a useful strategy for inviting smaller companies.

Investments related to core fibre network will continue to be in demand, says the Deloitte report. In India, this holds especially true with the large scope for rural penetration, currently at 57 per cent. Huge amounts will still need to be invested. According to Equitymaster telecom sector report in March 2018: “Given the low tariff environment and relatively low rural and semi urban penetration levels, demand will continue to remain high in the foreseeable future across all the segments.”

Also, the Modi government understands the potential of the sector in creating economic value and also direct and indirect jobs. Economic Survey 2017-18 had summarised the government’s aspirations thus: “Despite various bottlenecks, the Government is committed to extending the reach of telecom network to the remote and rural villages; …implementing the flagship ‘Bharat Net’ project, to link each of the 2.5 lakh Gram Panchayats of India through optical fibre network…the first pillar of Digital India Programme.

“It will facilitate the delivery of various e-Services and applications including e-health, e-education, e-governance and e-commerce. Major themes that new Telecom Policy shall try to address include Regulatory & Licensing frameworks impacting the sector, Connectivity for All, Quality of Services, Ease of Doing Business and Absorption of New Technologies including 5G and Internet of Things.”

There have been talks about plans to auction the 5G spectrum in bands like 3,300 MHz and 3,400 MHz to promote initiatives like IoT, machine-to-machine communications, instant high-definition video transfer as well as its Smart Cities initiative.

Because of the critical nature of the sector for the government’s Connect India and Propel India programmes, the sector needs to be supported. Interestingly, if the charges and levies are reduced, the companies’ ability to repay loans to banks and government increases – the government thus takes money from the left pocket and puts it into the right pocket.

With the government thus in their pockets, the companies need to act like partners to the government in connecting and propelling India; this will entail more and more imaginative solutions to problems that exist in the country, as also providing – importantly – better quality connections.

Swati Kamal is a columnist for Swarajya.

Get Swarajya in your inbox.

Magazine