Economy

Never Mind The Perma-Hawks And Fiscal Deficit: Expansion Of Government Expenditure Matters The Most Now

Karan Bhasin

Dec 26, 2019, 04:18 PM | Updated 04:18 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

The Union Budget is just a month away and wish-lists are prepared for the consideration of Finance Minister Nirmala Sitharaman. It is that time of the year where everyone is excited to know what is in store, more so because of the current economic slowdown.

This renewed interest has resulted in reignition of an old debate on fiscal deficits.

Perma-hawks have advised against deviation from the deficit targets however, many, including myself, continue to advise against rigid fiscal deficit norms — more so at times of economic slowdown. We look at fiscal deficits below and attempt to conclusively explain why they don’t matter.

Fiscal Deficits Don’t ‘Crowd’ Out

One reason why many believe fiscal deficits to be bad is because they crowd out investments. The argument of deficits crowding out investment comes from the impact of borrowings on interest rates.

However, the crowding out effect is relevant for closed economies, which have limited access to foreign funds.

In the case of India, it has been repeatedly found that government investments in fact crown in private investments.

The logic for this is quite intuitive. Public infrastructure usually is in the form of development of roads, rail networks or other physical infrastructure which is necessary for development of a region.

Therefore, the impact of fiscal deficits used for funding infrastructure may be positive rather than negative. This follows from the fact that private investors require some basic infrastructure to be able to undertake any investments.

Interestingly, many who advocate against the sovereign bond also argue against a fiscal expansion citing how it will absorb a bulk of domestic savings thereby reducing the availability of funds for private sector.

However, going for a sovereign issuance would resolve this problem and therefore, an opposition to both seems like contradictory. In many ways, an opposition to both is driven by inherent beliefs and a sense of risk aversion.

Fiscal Deficits Aren’t Always Inflationary

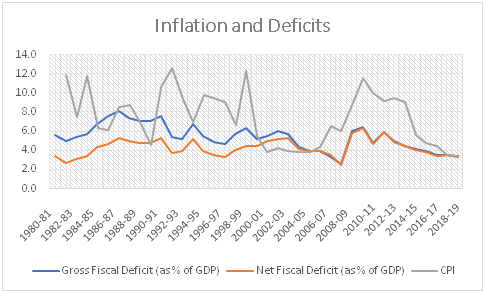

In the case of India, it has been the case that fiscal deficits and inflation have coexisted during different periods and many believe a strong link exists between these two variables.

However, not all fiscal deficits tend to be inflationary and a lot of it depends on the composition of fiscal deficits. That is, if one considers utilisation of the deficits for the purpose of meeting investment needs of the economy then it is less likely to be inflationary than compared to a scheme that aims at offering farm loan waivers or any such policy.

It is also important to recognise that a bulk of the inflationary impulse in the recent past was driven by the extremely high commodity prices including domestic food prices.

There have been times when inflation has been muted despite high deficits and inflation has also been high despite low deficits.

Another important point is that while some commentators mention how India’s actual fiscal deficit is high and a lot of the borrowings have been off the books, one wonders why the high fiscal deficit hasn’t impacted inflation which has indeed moderated substantially over the last couple of years.

The fact is that the relationship between deficits and inflation is not a simple one.

Moreover, till the time India’s output gap is negative, fiscal deficits are unlikely to result in inflation as demand will be weaker.

On the potential growth rate, it is important to recognise that while many believe India’s potential growth may have slowed to 6.5 per cent over the year, there is more evidence to suggest that our potential growth hasn’t changed.

This goes back to the structural-cyclical slowdown and the fact that there is a balance sheet problem doesn’t imply a change in the long-term potential growth rate of the economy.

In fact, it is very likely that this growth rate would have improved to 7.2 per cent — or that it would over the next couple of quarters. This follows from the J-Curve effect of reforms where in the initial years we witness a negative impact while it is only after some time that the economy experiences positive impact of these reforms.

Nobody can deny that both goods and services tax (GST) and Insolvency and Bankruptcy Code (IBC) are reforms —although of course both may be work in progress.

The GST does require some more thought going forward but irrespective, it combined with the IBC must have a positive impact on the potential growth rate and it is this positive impact that makes one believe that there is considerable room for monetary and fiscal policy to address such a wide output gap.

Only when we experience a positive output gap is when we should expect an inflationary impact of either monetary of fiscal interventions. Until then, whatever happens to inflation is determined by the rain gods and other seasonal factors.

This in turn reminds us of how Paul Volcker forced two recessions by monetary tightening in order to control inflation in the US which was largely driven by inflation expectations and uncertainty post the collapse of the Gold Standard.

This is an important lesson regarding the costs of using monetary policy to address an inflationary impulse at a time when there is a negative output gap.

Fiscal Deficits, Domestic Savings And Interest Rates

The impact of fiscal deficits on interest rates is of interest as increased government borrowings do tend to absorb domestic savings and put an upward pressure on interest rates. This happens primarily in closed economies that are capital deficient, but it also happens in the case of India because we have been too reluctant to borrow from external sources.

Consequently, we have artificially kept out domestic savings rates high and cost of capital higher thanks to our public finance policies, which has adversely impacted our competitiveness in the international market.

In 2007, India International Centre published the Mid-Year Review of the Economy 2006-07: India at a Structural Break authored by Surjit S Bhalla, Rohit Chawdhry and Tirthatanmoy Das. Chapter 7 of the book discusses India’s public finances and it highlights the extent of fiscal recklessness enabled by the ability of the states to borrow from the people in the form of postal ‘savings’.

Indeed, our public finance policies in the past, especially the late 1970s and early 1980s have been too indulgent and a repeat of this was even experienced in 2011. A high fiscal deficit does indeed result in absorption of domestic savings and increasing in the cost of capital but, not always.

Given that India’s inflation is significantly lower than before, our interest rates ought to be lower too.

This includes the small savings rates which are administered by the Ministry of Finance. A fiscal expansion at a time when monetary policy is accommodative, and the central bank is cutting rates can ensure that the cost of capital is reduced.

Therefore, greater coordination between the two main macroeconomic policies is needed to ensure the same.

Regarding inadequate domestic savings, while India is relaxing the norms for external commercial borrowings and there is a decent inflow of foreign capital, we need to seriously revisit the idea of sovereign bonds.

The huge divergence between India’s fiscal and primary deficit reflects the urgency to bring down our cost of capital and a sovereign issuance would help us achieve precisely the same.

The idea was a revolutionary one as it signalled a significant departure from our conventional understanding — it was the biggest idea in the previous budget, but it is yet to happen. One hopes that 2020 will see India’s first sovereign issuance.

For concerns of government getting into the habit of sourcing cheap funds from external sources, we can reform the Fiscal Responsibility and Budget Management (FRBM) Act or put in place reasonable restrictions on the percentage of debt that can be held by external investors.

Interestingly, the mid-year review also provides with a definitive and strong relation between cost of capital and investment. This is particularly relevant for many who repeatedly questioned my assessment of a stronger monetary action to address the current slump.

Their argument of ineffectiveness of monetary policy came from the developed world, which already had low levels of nominal and real rates, which was in contrast with India, which had high rates of both real and nominal rates.

As it turns out, some of them have eventually come around the view that India does need a monetary response as they argue for even stronger response from the central bank than what was argued by me some months back.

An unlikely consensus seems to have emerged on the need for serious monetary action while 12 months there were only a handful of economists who were arguing for the same.

Fiscal Deficits And Growth

The relationship between fiscal deficits and growth is a positive one and nearly everyone would acknowledge that deficits do have the potential to have a positive impact on economic growth in the short run.

Aggregate demand can be broadly summed up into four components, international demand for domestic products, demand for investments, government consumption and household consumption.

This broad classification is important for understanding why a fiscal deficit is important. Demand for investments depends primarily on the overall capacity utilisation and to some extent on cost of capital — that is, interest rates.

Therefore, in the event of spare capacity due to weak demand, simulating investment demand becomes difficult.

This in turn has an adverse impact on the growth of an economy which invariably results in households becoming cautious in terms of their expenditure which further weakens demand. This is a vicious circle and it needs to be broken by adequate policy intervention that drives demand.

Now international demand for our goods and services or exports is not entirely in the hands of the government as they depend on multiple factors (including exchange rates).

Similarly, private investment and consumption is likely to respond to higher growth, and therefore, these variables are also endogenous in nature.

In Keynesian sense, deficits are exogenous, and therefore, augmenting government demand for goods and services can help in breaking this cycle.

There are many who are arguing against a fiscal expansion now, however, given that our primary deficit is less than 1 per cent of the gross domestic product (GDP), one must really look at expansion of government revenue while reducing the interest costs of our past borrowings.

The case for an expansion of government expenditure can’t be any stronger than what it currently is, and therefore, one hopes that the government would recognise the same and do the needful.

Get Swarajya in your inbox.

Magazine