Economy

Nirmala Sitharaman Is Correct In Pitching For Lowering Interest Rates

Muthuraman

Aug 28, 2016, 11:28 AM | Updated 11:28 AM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

On 24 August 2016, Union Minister Nirmala Sitharaman set the cat among the pigeons when she said she would recommend a two percent reduction in interest rates. She said it would especially benefit the micro, small and medium enterprises (MSMEs) in the country. “I still hold that the cost of credit in India is high. Undoubtedly, particularly MSMEs which create a lot of jobs contribute to exports... are all hard pressed for money and for them, approaching a bank is no solution because of the prevailing rate of interest. I have no hesitation to say, yes 200 bps, I would strongly recommend,” she is reported to have said.

Swarajya carried an opinion this past week (26 August 2016) arguing how lowering interest rates would prove disastrous for the Indian economy. This article takes a closer look at the arguments placed in that opinion piece and provides data and analysis to counter many of them. It also aims to highlight the benefits that the banking system and the economy would accrue because of lower rates.

Please no shooting off the retirees’ shoulders

A common refrain against lowering interest rates is the impact it would have on retirees who depend on interest income in the evening of their lives. What is left unsaid is this: Less than three and a half percent of the total deposits in the banking system are estimated to be term deposits from senior citizens. There are enough tools in the hands of the government to safeguard retirees, some of which it is already using. These include higher tax slabs for retirees and even higher for super senior citizens and Varishtha Pension Bima Yojana. If more measures are required to be taken, the government (through banks or post office) can also launch special deposit schemes for retirees and subsidise the differential interest. Is it fair to hold the entire economy to ransom to support this three and a half percent?

The bogeyman of household savers

Let us address the common myth about household savings in bank deposits. Only 28 percent of the banking system deposits are term deposits from household savings (Rs 25 lakh crore out of Rs 89 lakh crore). The rest is from corporates, state governments, insurance companies, mutual funds, trusts, educational and religious institutions, etc., and balances in savings bank accounts and current accounts.

This is not to say that this large constituency should be ignored. But the Reserve Bank of India has to strike a balance between the interests of household savers and the cost of acquiring funds for entrepreneurs.

Credit risk spread largely independent of interest rate regime

The other argument put forth for not reducing interest rates is that the banks are facing high levels of non-performing assets (NPAs) and, therefore, have to charge a higher credit risk premium to make up for the loss. This is a specious argument because whereas credit risk premium is a spread over the risk-free rate, the interest rate reduction argument is for the risk-free rate. If anything, a lower interest rate to borrowers would make more units and projects viable, and improve the NPA scenario. As per recent reports, incremental addition to NPAs has started coming down, indicating that the worst is behind us.

Real interest rates are at decadal high

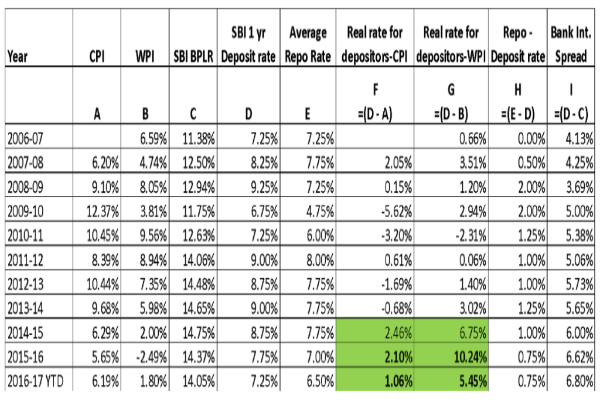

Real interest rates (based on both the consumer price index (CPI) and wholesale price index (WPI)) are at decadal high levels in the last two years, thanks to the largesses of the outgoing RBI Governor, Raghuram Rajan. (Please refer cells highlighted in green in Columns F and G in the table below).

(Sources: CPI, WPI index values, SBI PLR, SBI deposit rates, average repo rate)

As can be observed from the table, the depositors in the country have lived with negative real interest rates (State Bank of India, one-year deposit rate – CPI inflation rate) averaging at -1.20 percent between 2006 to 2014. This has turned positive two percent (and much higher at over five percent if WPI is used) in the last two years mainly because of Raghuram Rajan’s refusal to drop interest rates much during this period, despite the sharp reduction in both CPI and WPI (columns A and B).

Inflation has been managed remarkably well by the Modi government, largely by risking political capital in maintaining reasonable minimum support prices for agricultural produce. The benefit of this is not being allowed to pass on to the economy artificially by RBI’s insistence on holding the rates high, and it is high time it does so.

Inflation expectations are benign; timing is right for lowering rates

The inflation expectations for the coming quarters are generally benign, and Rajan also has clearly articulated this view recently. The global commodity rates are not going up anytime soon given the global economic climate, and oil prices are likely to remain muted, with the good monsoon recorded this year boding well for the softening of food prices.

While it is unfair to argue for sustained negative real interest rates, the average CPI inflation in the last 12 months is only 5.73 percent, compared to one-year deposit rates of 7.25 percent (which is closely correlated to repo rates). So there is definitely an elbow room for a reduction of 100-150 bps now and further based on the movement in CPI/WPI in the coming quarters.

A reduction in interest rates will also present an opportunity for the banks to strengthen their balance sheets through one-time mark-to-market gains from their G-sec portfolio. This can be used to offset the provisioning for bad debts, and help banks come out of the current mess faster.

Lastly, the fear-mongering of “lower rates leading to higher savings by household and retirees”, which in turn could lead to lower consumption, is largely unfounded and unsupported by much empirical evidence in India. As mentioned earlier, less than 30 percent of bank deposits are from term deposits of households and retirees. On the other hand, a large section of the population – households, SMEs and large corporates – are net borrowers for housing loans, vehicle loans and business loans. A reduction in interest rate would reduce EMIs for new loans and also leave higher disposable incomes in their hands, which will more than compensate for any reduced consumption by the retirees.

N Muthuraman runs Riverbridge, a boutique investment banking firm. He was formerly the director of ratings at CRISIL, India’s premier ratings firm

Get Swarajya in your inbox.

Magazine