Magazine

Will 2019 Be A 1929?– Part II

Shanmuganathan Nagasundaram

Jun 03, 2019, 01:52 PM | Updated 01:52 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

When I wrote the first part of this series for the January 2019 issue, there were few takers for the forecasts made. The consensus at that point in time for 2019 was for a strong gross domestic product (GDP) growth in the US, two hikes of 25 basis points each by the US Fed and quantitative tightening (QT) to continue on an autopilot mode at $50 billion a month. It was not even conceivable to the average reader to talk of a recession, let alone a depression, when the US Fed seemed to be at the early stages of a tightening cycle.

There will still be just a few takers for the dire forecasts that I continue to make as part of this series. But just a short five months down the line after the first article, the consensus on the monetary front has changed dramatically. The forecasts are now for zero hikes by the Fed for the rest of 2019 and QT has already been discontinued. In fact, more analysts now believe that the next Fed move will be a rate cut rather than a raise. This near 180 degree change in the monetary policy direction by Jerome Powell is now infamously referred to as the Powell Pivot.

Before continuing further, let me summarise the January 2019 article for the understanding of readers. The essential points were the following:

The US economy has largely been supported by simultaneous bubbles in several asset classes (equity, bonds and real estate) which have been sustained by the artificially low interest rate environment maintained by the US Fed for more than a decade since the GFC (global financial crisis). Looking at it through the prism of Austrian economics, a more accurate description of the US economic condition would be as a ‘dollar bubble’. That said, I presume, for the average person, it’s much easier to grasp a bubble in asset classes rather than a currency.

This state of ‘unstable equilibrium’ could easily be pushed past the tipping point with the bursting of any of these bubbles or by any exogenous/black swan event. The ensuing recession would be more prolonged and severe as compared to the GFC. In fact, as I point out, just as the markets would try to liquidate the massive bubbles through deflation, the US Fed would try to prevent it through their inflationary tools of zero interest rate policy (ZIRP) and quantitative easing (QE).

To wit, QE in perpetuity would send the US economy into an inflationary depression which could last a decade or longer — a period that eventually would be referred to as ‘The Greater Depression’. The US dollar is consequently going to lose a substantial portion of its purchasing power over this period.

Before I proceed to make the point as to why the events of the last few months continue to make the case for the above stronger, it’s worthwhile to explain the strong 3.2 per cent 2019 first quarter GDP growth in the US. The subsequent (Donald) Trump claims of “at the end of six years, you’re going to be left with the strongest country you’ve ever had”, are going to make former Fed chief Ben Bernanke’s claims prior to the GFC (January 2008 — “The US Fed is not currently forecasting a recession”) appear like a misdemeanour in comparison.

The first quarter GDP had a number of one-offs. Without the import payback and the inventory gains, the GDP growth would have been sub 2 per cent. Both these are statistical aberrations that not only will not repeat themselves for the rest of the year, but in fact would go on to dampen the GDP growth for the rest of the year. Add to this the annualised GDP deflator of just 0.9 per cent in a period in which oil prices had witnessed a surge of more than 30 per cent on a quarterly basis, one can only conclude that the GDP growth mirage would be just that — a mirage.

But not to belabour Trump’s supposed GDP achievements too much, my contention is that there will essentially be a discontinuity in the GDP trends at some point. Once the recession takes hold, the levels of debt within the system and the ensuing massive fiscal stimulus for which there would be a shared consensus amongst the Republicans and Democrats, would cause a flight away from treasuries. This would send interest rates soaring northwards and would essentially sound the death-knell for all the three bubbles — equities, bonds and real estate.

What are the reasons as to why I believe we might well be on the verge of that tipping point right now? Readers should remember that GDP estimates are a lagging indicator and typically a recession is recognised a good three to six months after it actually starts. Even the GFC of 2008 was not acknowledged well after the crippling events had taken complete control of the economy. It indeed is probable that the US will enter ‘The Greater Depression’ (GD) in second quarter/third quarter of 2019, though even the recession let alone the GD, will not be acknowledged till perhaps well into 2020.

What are the leading indicators that make me believe that the US economy might well be entering a recession right now?

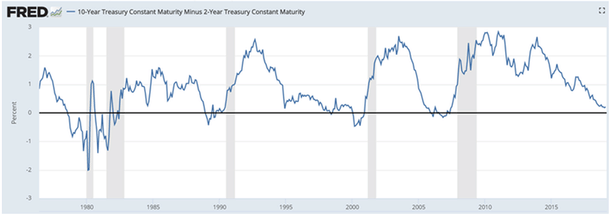

The Yield Curve Inversion

The yield curve is a graph that plots the interest rate yield on bonds over varying maturities. In general, bonds of a longer tenure (typically 10 years) would have a higher yield as compared to bonds of a shorter tenure (three months to two years) to compensate for the additional risk associated with the longer tenure. The above graph shows the difference in yields between a 10-year and 2-year treasury.

When the above graph falls below zero it means that the short-term yields are greater than the long-term yields. The shaded areas are economic recessions and historically this inversion has been one of the best predictors of recessions. It indicates that the markets expect their central bank to cut interest rates that would cause the short-term interest rates also to decline reversing the inversion.

As I had said in the first part of the article, not only do I expect the Fed to cut rates aggressively but to actually go back to ZIRP as well QEs over the next year or two.

The Political Clamour For Rate Cuts, QEs And Deficits

It’s one thing for the markets to indicate the future direction of interest rates through an inversion of the yield curve. But when President Trump and the Director of National Economic Council, Larry Kudlow, demand immediate rate cuts of a large magnitude, it’s an entirely another matter.

Why would they demand a rate cut and a return to QE at a time when the US GDP growth is supposedly at its best record in recent times and unemployment rate at a 50-year low? Trump, in fact, has demanded that the US Fed cut rates by 100 bps. The last time the fed cut rates to that extent in a short time was during December 2008. Why would Trump want the US Fed to mimic an act that was performed at the depths of the GFC?

Not only are they demanding the cuts but the fiscal deficits are now surpassing the levels of what would be classified as a stimulus under recessionary conditions. Even the most rabid Keynesian would shudder at the thoughts of a $1.2 trillion deficit during the tenth year of a business expansionary cycle. The question to be asked is, why so? Leave Trump aside as he may not understand much of economics but why would a supposedly fiscal conservative such as Kudlow advocate massive deficits towards the tail end of a cycle? And if these are the deficits during good times, what’s going to be the size of the deficits in the oncoming recession? My guess — north of $2.5 trillion.

As I will show below, there’s sufficient evidence to believe that the US housing, retail and the autos might well have already rolled over into the recessionary territory. Being aware that it’s pretty much impossible to reverse the recession in short order, Trump and company are actually trying to postpone the recession — perhaps till the next election cycle. Hence the preemptive demand for a large cut in interest rates as well as restarting QEs.

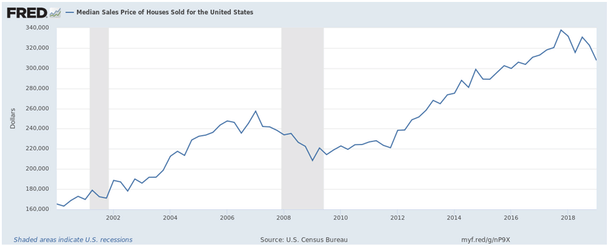

Housing Bubble 2.0

Most individual wealth-creating statistics, such as the number of labour hours worked, median incomes, etc., are barely above the GFC levels even today. However, median housing prices have recorded an impressive near 40 per cent gain from their pre-GFC peak levels during the fourth quarter of 2017. Then coinciding, again not coincidentally, with the marginal increase in rates by the US Fed, housing prices started to decline and this has continued despite the Powell Pivot earlier this year.

Other statistics tend to confirm the beginning of the housing bubble 2.0 bust as well. We have had six months of consecutive year-on-year declines in residential construction spending and this despite long-term rates being lower today as compared to a year ago. Besides, FICO scores of purchasers have also been relaxed, a pattern uncannily similar to that of the lax lending standards of housing bubble 1.0 — a pattern that was previously witnessed just prior to the GFC.

I am sure analysts would make an argument that it is different this time and that we do not have a sub-prime category as we had prior to the GFC. My point is that if the median incomes have not changed substantially, and if median housing prices are up substantially, then there’s a large part of the housing loan segment that is begging to be reclassified as ‘sub-prime’. We may not have to wait more than six to 12 months to find out what accounting tricks have been deployed this time around to hide those borrowers.

Autos, Retail Declining

Again, housing is not an isolated issue. We see a similar pattern with auto sales declining on a year-on-year basis, inventories of finished cars running at seven-year highs. A similar trend has been observed in delinquencies on auto and credit card loans.

Retail store closures also seem to be on an accelerating path in 2019. The first four months of 2019 witnessed more than 6,000 store closures compared to 5800+ for the entirety of 2018. This trend is expected to continue for a projected closure of 12,000+ stores for 2019. I could provide several other statistics, but I presume the recessionary trends are clear.

How does one reconcile the above on-the-ground numbers with the lowest unemployment levels in 50 years? Candidate Trump did have an insight on this issue when he pointed out that “unemployment numbers are fake” and that the labour force participation rate is at its lowest levels ever. With the number of unemployed Americans recently crossing the 100 million mark for the first time ever, there indeed is a deeper malaise that the headline unemployment numbers conveniently mask.

The End Game

It’s hard to come to any other conclusion other than that we are at an epochal moment in the monetary history of the US dollar. Or what Austrian economists would prefer to see as the road leading up to a ‘crack-up boom’. Whether that crisis starts in 2019 or 2020 is probably not too relevant other than from the perspective of a near-term speculator.

The incumbents at either end of the Accela Corridor seem to be clueless on the nature of the crisis that lies ahead. To that extent, we will have exactly the wrong diagnosis when the crisis erupts resulting in the monetary response of ZIRP and QEs which would give us the inflationary depression scenario discussed earlier.

The excesses that have been built into the system in the form of debt, credit and unfunded liabilities are way too excessive and something that would have never occurred under a gold standard. But apparently, every generation has to learn the hard way that the monetary king of fiat money is indeed naked. As history has repeatedly shown, perhaps hundreds of times, the only sustainable monetary standard is to abolish central banks and return the function of determining the quantity of money and the price thereof (i.e. interest rates) to the free markets.

But why will an institution (i.e. government) to whom the citizens have voluntarily bequeathed the monopoly use of force against themselves be expected to voluntarily relinquish the monopoly use of the printing press? An orderly transition to a sustainable solution is anything but conceivable.

Shanmuganathan N (aka Shan) is an Economist based in India. He is the author of the recently published book "RIP U$D: 1971-202X …and the Way Forward" and can be contacted at shan@plus43capital.com

Get Swarajya in your inbox.

Magazine