World

Explained: Where Did It Go All Wrong For Sri Lanka's Economy

- Sri Lanka has a debt addiction, and it cannot be attributed to China alone.

- The debt addiction problem is compounded by structural weaknesses within the economy which include a lack of foreign investments, negligible expansion of a tax base, and failure to expand the exports.

Economic crisis in Sri Lanka

Protesters on the road, a developing law and order situation with citizens directly in conflict against the forces, one of the houses of the Prime Minister being torched, prolonged power cuts, lack of food, inflated costs of all the necessities, downgraded sovereign rating by most international agencies, almost negligible foreign reserves, dented tax revenues due to the pandemic with faltering exports, and a soaring public debt that has rendered the existence of the Rajapaksa lobby futile and has ushered the fall of the government.

One wonders, where did it go all wrong for Sri Lanka?

The clouds of economic doom were visible in early 2021 itself when international agencies began citing the government’s weak fiscal situation as a reason for downgrading them. S&P Global Ratings downgraded Sri Lanka's long-term sovereign credit ratings to CCC+/C from B-/B, stating that the pandemic had ravaged the island nation’s revenues and therefore, servicing the debt would be an issue.

Moody’s also cited the external factors, including weak revenue from textile and garment exports and lowered remittances, to downgrade Sri Lanka’s ratings. The Sri Lankan government, however, back in 2021, dismissed these predictions as baseless.

The island nation has a debt addiction, and it cannot be attributed to China alone, for the monetary support from Beijing is relatively a recent phenomenon. The debt addiction problem is compounded by structural weaknesses within the economy which include a lack of foreign investments, negligible expansion of a tax base, and failure to expand the exports.

The pandemic, which dented tourism across the globe, a critical source of revenue for Sri Lanka, and the recent war in Ukraine, which sent the crude prices for a toss, only worsened the problems for the Rajapaksa regime. Simply put, Sri Lankans were cashing more debt than their revenues could service. The pandemic, resulting in low oil prices, curbed Sri Lanka’s capital outflows, by almost $1.35 billion, but the temporary fall in crude prices was not going to delay the inevitable economic crisis.

If one looks at the debt-to-GDP ratio for the last half-century for Sri Lanka, a pattern of dependency on loans emerges. Across the 1970s and 1980s, the public debt steadily increased, with a significant increase in foreign debt, before peaking in the late 1980s when the public debt (foreign and domestic combined) was more than 100 per cent of the GDP. The foreign debt levels, as a percentage of the GDP, have actually decreased since the late 1980s, going as low as 30-odd per cent in 2014, compared to 60 per cent in 1988. So, why all the trouble now?

Across the 1990s, Sri Lanka’s foreign debt was made up of concessionary loans, sourced from the likes of the World Bank, and Asian Development Bank and they came with a long payback period and low-interest rates, giving the government a strong cushion for repayment. Thus, at that point, the foreign debt, payable after 20 years, minimum, was not at all a threat to the servicing capacity of Sri Lanka.

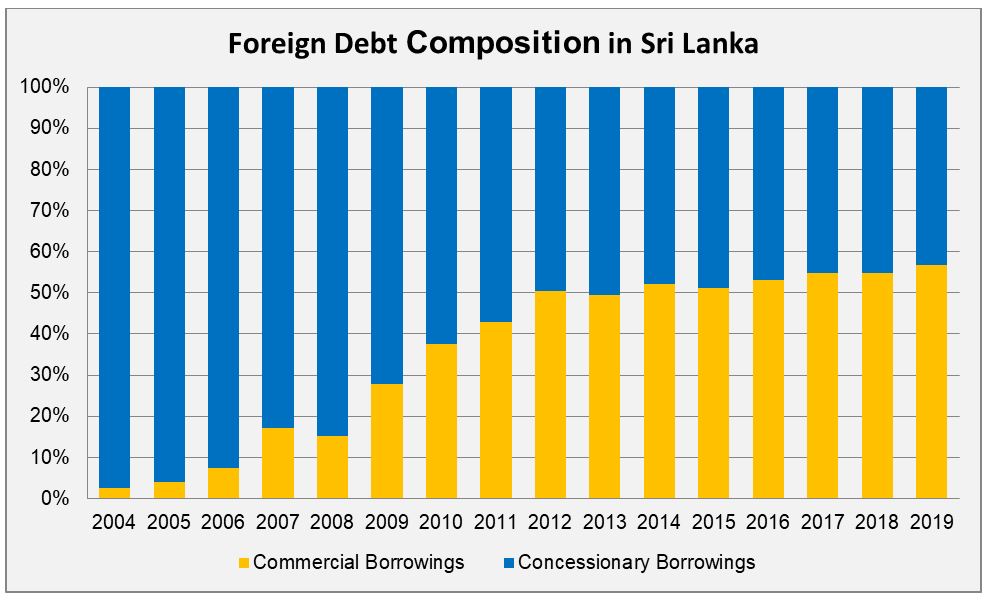

However, as is the case with the all free lunches, the concessionary loan spree also came to an end in the 2000s and the country had to move towards commercial borrowings with a significantly higher rate of interest, and without the ease of payback. This is where the problem began.

{kind=link}

As per the data of Sri Lanka’s Central Bank, in 2004, commercial borrowings made up less than 5 per cent of the total foreign debt with over 95 per cent of foreign debt in concessionary loans. By 2010, commercial borrowings were close to 40 per cent of Sri Lanka’s foreign debt, and by 2019, more than 55 per cent.

The commercial borrowings were in the form of ISBs or International Sovereign Bonds that were used to raise money from the global markets. Usually, these bonds matured after 5-10 years, and also had an interest payment that was to be made regularly. As the bonds matured, the foreign debt only increased, and with every bond payment, a large outflow of foreign exchange was also happening.

For instance, Sri Lanka has an ISB worth a billion dollars maturing in July 2022. Meanwhile, all these years, the debt was growing, but the economy was not.

The International Monetary Fund (IMF) had to bail out Sri Lanka on two separate occasions. Once, in 2009 when the economy was struggling due to the global financial crisis. The IMF loaned $2.6 billion to the island nation, stating that it was to help the country’s short-term needs and the impending balance of payments situation. Back in 2009 as well, Sri Lanka’s exports suffered due to the crisis, especially those of tea and textiles, and capital outflows. Yet, across the 2010s, the governments in the country failed to address the structural problems.

In 2016, the IMF had to again come to the rescue of Sri Lanka, with a loan of $1.5 billion. This time, the balance of payments crisis had been triggered by huge capital outflows due to the servicing of foreign debt and maturing bonds.

Cut to 2022, and the Sri Lankan government, given its poor ratings, cannot go back to the tried and tested formula of ISBs to raise money from the financial markets. In April, the government suspended all payments on foreign debt, raising concerns amongst the investors. There are reports that the government will look for assistance from the IMF, yet again, and restructure its foreign debt.

There were also reports of the Sri Lankan government using the IMF loan, in 2022, to temporarily ward off the bondholders before re-negotiating the values of the bonds with them.

Sri Lanka’s own economic ‘wokeism’ has also added to its woes. In April 2021, the Sri Lankan government banned the import and usage of synthetic fertilisers and decided to go organic. For an island nation, dependent on agri-exports, and with more than 60 per cent population directly or indirectly dependent on farming, the move was economically suicidal.

Thus, Sri Lanka, had to now worry about food security, was importing rice, and was unable to export as much tea as it was doing before. The yield (tonnes/hectare) fell from 4.85 in 2019-20 to 4.57 in 2020-21 to 3.91 in 2021-22. The production came down to 2.92 million tonnes in 2021-22 from 3.39 million tonnes the previous year. The imports increased more than four times, from 147 thousand tonnes in 2020-21 to 650 thousand tonnes in 2021-22. The rice import for 2021-22 was more than that between 2017-2021 combined. Hail Organic!

Sri Lanka, much to the dismay of many Twitter economists in India, also went on a money printing spree and had to witness the music slowing down. The premise behind printing more currency was to increase the share of the domestic debt against foreign debt, which the Central Bank head believed would not be a cause of concern.

Thus, between December 2019 and August 2021, the money supply increased by 2.8 trillion Sri Lankan rupees, a whopping 42 per cent. Today, the island nation battles with consequent inflation, as high as 19 per cent, even for the most essential commodities.

The 'wokenomics' history does not stop there, for the Rajapaksa government, after taking over in 2019, went on tax cuts, reducing the value-added tax to 8 per cent from 15 per cent, and doing away with the 2 per cent tax on domestic goods and services. Compared to 2019, there was a 30-odd per cent decrease in tax income for the government.

The pandemic in 2020 was the final nail in the coffin. Tax revenue as per cent of the GDP has fallen to 8-odd per cent, the lowest in two decades. The lack of funds to pay for oil imports has resulted in power cuts that range from four to twelve hours each day.

Where does China feature in all this, for it has often been speculated that Sri Lanka’s economic mess is a result of the debt-trap diplomacy of Beijing? Turns out, that China makes up for one-fifth of Sri Lanka’s current debt, but over one-third of the debt comes from the commercial borrowings that began in the early 2000s. That is where the story of Sri Lanka’s economic doom begins.

Thus, even if China were to restructure its debt, take over all the infrastructure projects it has invested in, or, for argument, were to let go of the debt, the challenges for the Sri Lankan economy would remain. In the following years, 50 per cent of the public debt in the nation would be to service the ISBs. China or no China, without structural fixes, Sri Lanka’s economy is in an uncontrolled spiral downwards.

To sum it up, therefore, first, it was the ease of borrowing, thanks to the long payback periods and low-interest rates. When the ease evaporated in the early 2000s, commercial borrowing through ISBs was preferred, in the hope that the debt-fuelled economy would create enough revenue to pay off the bonds.

The economic growth, more than 8 per cent post-2008 and until 2012, validated this hope, and the borrowings only increased. In 2013, the growth rate fell to 3.4 per cent, and before peaking at 5 per cent in 2014 and 2015, fell to 2.4 per cent in 2019. Between 2004 and 2020, exports, as a percentage of the GDP, went from 35-odd to merely 16 per cent.

In 2019, economic wokeism took over as the state disrupted the agricultural sector, slashed taxes, and went on a printing spree. The pandemic contracted the economy in 2020 and 2021, as tourism was hit, and in 2022, with the crude oil prices hitting the roof, the cycle of economic doom was complete.

There is a lesson for politicians, fans of freebies, in India as well. To slash taxes or divert state resources towards fulfilling waivers is an idea that wins elections, but in the long run, only weakens the state. Free electricity or water may not pose a significant cost in the short-term but in an unprecedented global economic scenario, especially after the pandemic, things can go wrong quite quickly. Freebies are no governance model.

For Sri Lanka, the hope lies in an IMF bailout, long-term credit at low-interest rates from India and China, restructuring of existing debt and renegotiation with current bondholders and creditors, and most importantly, addressing the structural issues that have plagued their economy for a decade now to not repeat the mistakes of 2009, 2016, and 2019.

Introducing ElectionsHQ + 50 Ground Reports Project

The 2024 elections might seem easy to guess, but there are some important questions that shouldn't be missed.

Do freebies still sway voters? Do people prioritise infrastructure when voting? How will Punjab vote?

The answers to these questions provide great insights into where we, as a country, are headed in the years to come.

Swarajya is starting a project with an aim to do 50 solid ground stories and a smart commentary service on WhatsApp, a one-of-a-kind. We'd love your support during this election season.

Click below to contribute.

Latest