Business

Hindenburg… Or A Lead Zeppelin?

Rudra

Aug 12, 2024, 08:21 PM | Updated 09:54 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

To say that the actual report published by Hindenburg Research (HR) as the follow-up to this ominous tweet turned out to be a damp squib would be an understatement.

In the background to the report, HR alleges the lack of adequate action against the Adani Group by the Securities and Exchange Board of India (SEBI). It then appears to attribute this to some connection between the current SEBI Chairperson, Madhabi Puri Buch (MPB), and the Adanis. I quote from the report:

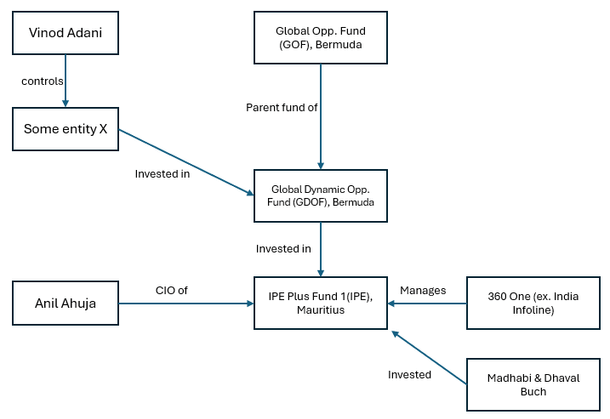

I have attempted to sketch the structure mentioned in the report below for clarity:

The key allegations expressed or implied (as I make out) are as follows:

1. Anil Ahuja is linked to the Adani Group, and he managed IPE; Adani may have invested in IPE.

2. MPB and Dhaval Buch (DB, MPB’s spouse) invested in IPE (“hidden stakes”), so MPB and DB are connected to the Adani Group.

3. And finally, what seems to be just thrown in for good measure: 360 One (360) is linked to the Wirecard fraud.(IPE-Plus Fund was owned by 360-One WAM, formerly IIFL Wealth Management)

Let’s examine each of these to the extent we can:

1. Anil Ahuja: He is linked to the Adani Group by virtue of his being on the board of Adani Enterprises for nine years. But that is not the entirety of his career. He was also on the board of HDFC Bank for six years. He is an IIT and IIM graduate and has also served as the VP of Citibank, CEO of JP Morgan Partners (Asia), and Asia head of 3i Group before taking on the role of Founder and CIO of IPE. A designation he held from 2014 to 2018. It would not be wrong to say that his stint with the Adani Group was just one of the things he did in a long and apparently successful career. Could he just be a front for someone? Anything is possible, but is it likely? Especially on the evidence provided in the report. Unlikely, in my opinion.

2. MPB/DB’s “stakes” in IPE: For one, I am not sure calling an investment in a fund can be characterised as a “stake,” which is suggestive of ownership or management. But let’s not go into semantics and instead see her entire dealing with the fund:

a. 5 June 2015: MPB/DB opens an account with IPE

b. 22 March 2017: Accounts transferred solely in DB’s name

c. April 2017: MB appointed as Whole Time Member of SEBI

d. 25 February 2018: Funds redeemed

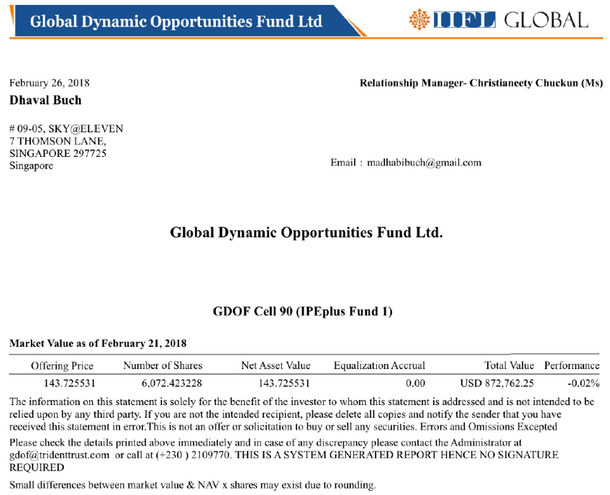

So, Madhabi opened her account with IIFL well before her appointment with SEBI. Did she make money from this investment? Not at all. In fact, the HR report itself links to a NAV statement for the fund dated 26 February 2018, which indicates a loss of 0.02 per cent:

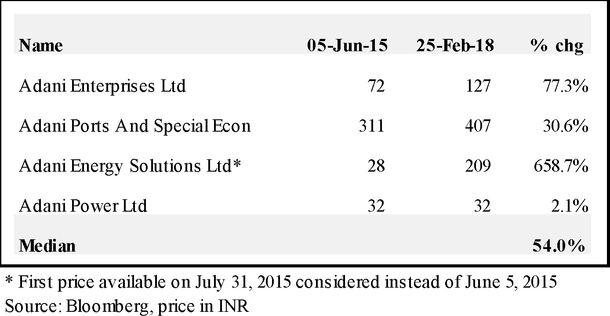

I do not know what the fund had invested in. But if the insinuation is that this fund was used to manipulate the Adani Group’s share price, it is a reasonable assumption that it should entirely or substantially consist of Adani Group shares, isn’t it? If so, the performance of this fund should mimic the performance of Adani Group shares. Let us examine how Adani Group shares performed during the duration of Madhabi’s investment in the fund:

As one can see, a cross-section of the major Adani Group companies returned a median 54 per cent during this period, a far cry from the flat performance of IPE that MPB/DB had invested in. As such, it is unlikely, in my opinion, that this fund invested only in or majorly in Adani shares.

In the context of this investment, Hindenburg makes a bizarre allegation about MPB that is as follows:

Basically saying, why did she invest in an offshore fund instead of having regular mutual fund products in India.

This is bizarre on two counts:

1. If the assets in IPE were “miniscule,” then how could that fund be used to manipulate the stock price of Adani Group shares and

2. If she didn’t break any laws in investing in this fund (HR doesn’t specify that she did), then she is free to diversify her investments as she sees fit. In fact, the documents uploaded by Hindenburg itself indicate that MPB/DB had a net worth of approximately US$10 million. So this investment of US$0.87 million is less than 9 per cent of their total asset base. Maybe this investment was just a diversification?

In light of the above document, it is worth noting that Hindenburg refers to her investment as a “hidden stake”:

If so, this would be an unusual case where a hidden stake has a name, identification number, address, source of money, and occupation disclosed and verified. If HR is insinuating that she had hidden this stake from some statutory disclosure in India, then they need to make that clearer with evidence. At least to me, it is not apparent.

In summary, we have what seems to be a completed KYC, no evidence of a regulatory breach in the ‘investing’ itself, and no money made from the investment. To call the link to Adani tenuous just because they may or may not have invested in the same fund as tenuous would be generous.

3. 360’s “reported ties” to Wirecard: The link that Hindenburg provides for this allegation is from a Financial Times article dated 30 March 2023. The relevant excerpt is reproduced below:

The crux: Amit Shah, a co-founder of a company called IIFL Wealth (now supposedly renamed 360 One), allegedly arranged for a company to be purchased for X amount, and just weeks later have it sold to Wirecard for 9X.

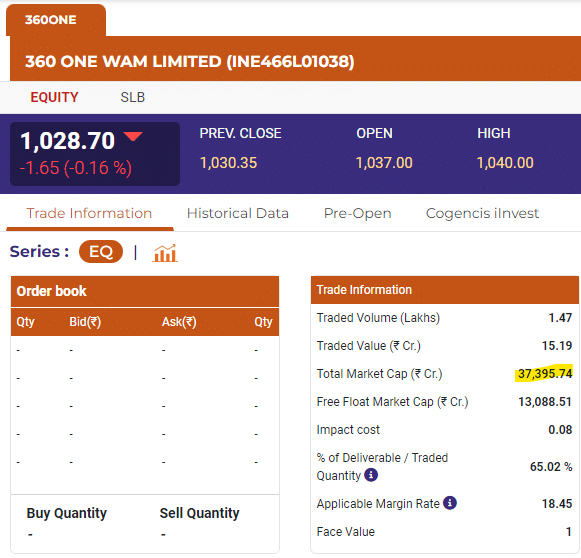

I don't know that case, nor do I make any comment on it. That is for the courts to decide. But 360 is a listed company with a market cap of Rs 37,395 crore. They may have many products for various clients (about 7,400 HNI and UHNI families per their 1QFY25 presentation). Are all those clients also now linked to Wirecard by this logic? Unlikely, in my humble opinion.

This covers the main set of allegations being made in the report. There are some side attractions as well.

1. MPB had a stake in a consultancy firm in Singapore called Agora Partners. She transferred the stake to her husband in March 2022, just after being made SEBI chair. Here I confess that I do not know the legality of a SEBI Whole Time Member or Chairperson having such a stake. If there is a specific violation of a rule, HR doesn’t seem to have quoted it. Securities lawyers are better suited to comment on this. Hindenburg does not have access to Agora Singapore’s financial statements either, making any judgement on this point baseless.

2. Finally, they seem to allege a few things about DB. They say that he joined Blackstone as a senior adviser, despite never having worked with a fund.

I may have misunderstood them, but if in fact they are insinuating that Blackstone hired him to get an “in” with the SEBI chair, then they should be addressing their queries to Blackstone or then providing proof of a direct quid pro quo. Additionally, it is worth mentioning that Daval was hired in 2019 (per HR’s article), while MPB became the Sebi chair only in March 2022.

Also, Dhaval was the Chief Procurement Officer of Unilever. Unilever is one of the largest consumer companies in the world, and procurement is critical to their operations. To paint him as someone who didn’t know the first thing about investing or funds is disingenuous, if indeed that is the attempt. There are several lateral hires, especially in the PE industry, to get access to industry expertise.

3. The last major allegation is that she urged investors to have a "positive" view on REITs, while Blackstone has forayed into Indian real estate. So, if MPB advocates investing in mutual funds, will they accuse her of shilling for one of her prior employers who runs MFs? I think this is a really stretched connection unless Hindenburg has some direct or even indirect proof of a quid pro quo. On a lighter note, if in fact anyone wanted to influence investors in India, they would do better to do it through some ‘finfluencer’ rather than the SEBI chair.

All in all, I am quite disappointed with the quality of arguments, corroboration, and lack of intellectual rigour in general that appears to have gone into making this report. I have no fundamental opposition to short sellers or to short selling. If it is done with honesty and intelligence, it can act as a check on unscrupulous promoters and lax regulators where needed. But insofar as I have read this report, and I have relied almost exclusively on it, this report falls short by quite a margin.

Get Swarajya in your inbox.

Magazine