Economics

Transaction Tax – an idea whose time has come

Anish

Jan 04, 2014, 04:38 PM | Updated Apr 29, 2016, 01:06 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Background:

Information is filtering through in bits and pieces in the media (mainly social media) about this new idea that BJP seems to be toying with. Primarily, people have got excited about the fact that one of its key precepts is to do away with income tax. Rumours that this would be included in the BJP manifesto and coupled with the general expectation that the NDA could be coming to power, has only added more fuel to the fire. There have been few statements made in the national media by Nitin Gadkari, Rajnath Singh and Subramanium Swamy on this, which has only further accentuated the curiosity. However, not much of an intellectual debate has taken place on this, although ostensibly, many people claim to have gone through the proposal (in detail), and some have even concluded that it is impractical!

The proposal has been formulated by an organization called Arthakranti and one can go through the details on their website (ARTHAKRANTI). This is an attempt to critically examine the proposal, look at its benefits and downsides (if any) and draw certain conclusions. My final opinion is that it is a good idea but needs a lot of work (nothing ever is fully baked at an ideational stage), and requires a full-fledged debate in the nation for understanding it and building a constituency for it. I also think that, quoting a cliché but nevertheless, this can be a game-changer idea for India, and should be implemented sooner rather than later.

Salient features of the Proposal:

The proposal that has been prepared by Arthakranti is very detailed and goes into many different areas, including how to change funding for political parties as well as creating a social security fund for BPL (Below Poverty Line) families. I am not commenting on these aspects, important enough as they may be on their own. I am focussing mainly on the changes in the tax-regime proposed and their economic and financial implications. I have also not independently validated the numbers presented by them, and am going with what they have put up on their website.

The key changes proposed are as follows:

- Abolish all Direct and Indirect taxes in the economy (including Income Tax, Sales Tax, Service Tax, etc.), except Customs Duty. Implicitly, this also means do not implement the GST, which has become an article of faith for Corporate India.

- Withdraw all high-value currency denominations in the economy, i.e. the highest denomination should be the 50-rupee note, and eliminate the 100-, 500- and 1000- rupee notes from the system.

- Introduce a new Banking Transaction Tax (BTT), to be levied at the rate of 2%, deductible by Banks on all non-cash transactions that pass through the banking system.

- Exempt all cash transactions from any form of tax, except that those transactions of value greater than INR 2000/-, would not enjoy “legal protection” (i.e. one cannot raise a legally valid invoice for this amount, nor can one enforce a transaction, if the amount was settled in cash and was greater than 2000 rupees).

- Distribute this 2% amount collected by the Banks (under BTT), in the following proportion:

- To the Central Government – 0.70%

- To the State Governments – 0.60%

- To the Local Governments (i.e. Municipalities and Panchayats) – 0.35%

- Retained by the Bank (as facilitation fees)– 0.35%

Direct Benefits:

The changes proposed above seem simplistic but will have far-reaching implications and direct benefits. The key ones are as follows:

- There will be a tremendous compression of costs in the economy (could be in the range of 20% -40%), as indirect taxes, which are a major cost, will get eliminated. This would make Indian manufacturing extremely competitive with China. This will have a multiplier-effect on services also, and provide a major boost to exports, bridging the trade deficit and strengthening the value of the Indian Rupee.

- There will be a huge improvement in consumer sentiment as expendable income in the hands of individual salary-earners could go up by 20% – 35%, as personal income tax would be eliminated.

- There will be a significant improvement in the investment climate as investible funds in the hands of corporates would go up by 25% – 40%, as corporate tax would be eliminated. This will give a huge impetus to capital formation in the economy as well as project investments.

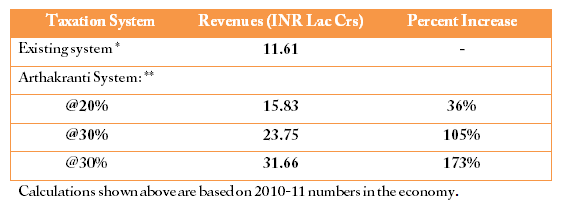

- There will be a significant increase in tax revenues to the government (both Centre and States), as shown in the following table below. This would also reduce the fiscal deficit and the debt burden (which has grown uncontrollably).

Revenues (both Central & State Governments) through tax collections

Calculations shown above are based on 2010-11 numbers in the economy.

* As per budget figures of FY 2010-11

** Based on different percentages of Daily Narrow Money (M1) in the banking system, which converts into banking transactions

Other Indirect Benefits:

There are many indirect benefits envisaged in this system, as follows:

- Tax compliance would improve dramatically as the “tax-saving” motivation for tax avoidance will totally collapse

- Significant portions of the parallel economy (which is estimated to be almost as large as the main “white” economy”) would move “above-ground”, as tax incidence would come down to a nearly insignificant 2%.

- An extremely high proportion of the cash transactions in the economy would move into the banking system, primarily because:

- It would become inconvenient to conduct “high-value” transactions if the highest denomination currency is a fifty-rupee note

- No legal protection would be available for a cash transaction if it is of a value greater than two thousand rupees (except for bribe-money, this would be useless for all other forms of transactions).

- The 2% BTT tax in the hands of the recipient is almost an insignificant amount of tax to save, to justify the efforts (and costs) associated with “hiding” that transaction from the Banking system (hence the 20% – 40% assumption of M1 money moving through the banking system appears to be conservative).

- This will be a death-blow to the “black-money hoarders” (which is largely done in high-value currency notes), as this would now become “waste-paper”. A one-time VCIS scheme might be an attractive option to bring out all this money into the legal economy.

- The pressure on the system to check and control fake currency notes floating in the economy would collapse as it is almost economically unviable to print and benefit from fake currencies if the value of the note is just fifty-rupees.

- Since the Banking system would get a new and significantly large revenue stream (estimated at INR 4.27 Lac Crores), the financial pressure on banks would come down, and hence bring down interest rates in the economy also.

- Inflationary pressures in the economy would ease considerably for the following reasons:

- Cost of production would come down significantly due to the elimination of taxes

- Fake currency notes in the system (which adds to money-supply and hence inflation) would disappear.

- Lower costs would spur new projects and hence capacity creation in the economy

- Alternative revenues streams for Banks would directly bring down interest rates

- Easing of pressure on the government to borrow from the market to bridge budget deficits, would reduce the overall fiscal deficit, because of buoyant tax revenues.

- A significant section of the economy (Agri-sector), which has for long got used to not paying any taxes, will now also get equivalently treated (as Manufacturing and Services sectors). This will also assuage feelings in the Middle Class as until now they have been disproportionately bearing the burden of direct taxes in the economy.

- India becoming a “low-tax” economy would become a magnet for FDI and FII inflows, which in turn would lead to a buoyant stock market, spurring economic activity and a return of the so-called “animal spirits”.

Risks and other imponderables:

There are many risks associated with this proposal as it is a new proposition, mainly as follows:

- No one has gone here before and in that sense this is a pioneering effort (although there are reports of some other countries exploring such proposals also). Recently, a similar proposal has been adapted by a US Senator and has been put up for a feasibility study in the U.S. (Ref – The Orator ) Another similar-sounding proposal has been put up by an American Professor, Dr. Edgar Fiege, primarily aimed at reducing complexities of the taxation system. (Apttax).

- Rural India, which is severely under-banked, would not be well-covered initially in this system. However, since this is largely a cash-based economy, they may have some issues because of low-value denominations, which might cause some inconvenience and delays. Banks would also be tempted to cover these areas in time, as it is a potential revenue stream for them.

- It is unclear whether the Indian banking system can take on the load of this high a number of transactions and also transferring these amounts into the government system. However, experience with credit cards, net-banking and RTGS, etc., would suggest that with a few early-stage hiccups, they can deliver.

- It is also unclear whether 20% – 40% of M1 money will flow in through banking transactions. Unfortunately the study does not give an indication of what the current volume of flows is in the system. However, as the disappearance of high-value currency notes takes effect, it will drive more transactions through the banking system; this should not be an issue.

- As high-value transactions become increasingly inconvenient, it could lead to other forms of distortions like barter-trades or using other “stores-of-value”, like gold. This is possible but cannot really be a very significant part of a trillion dollar economy, even if it becomes administratively uncontrollable.

Other Issues:

There are a few other attendant issues that could crop up as this proposal gets implemented:

- This could lead to a collapse of the traditional “tax-advisory” business, which is a significant chunk of the work that Chartered Accountants do. This could also lead to some resistance, and maybe even “fear-mongering”, which needs to be managed. Additionally, a significant new stream of work could get created in the area of “compliance audits”, i.e. whether banking transactions are leading to BTT revenues or not. This would require the profession to re-invent itself, which is not necessarily a bad thing.

- This could also make redundant the huge tax-collection machinery that the government has built up over the years. Eliminating the hard-infrastructure would be the easier part of the job. The soft-infrastructure in terms of people could be handled through a judicious mix of VRS and redeployment in other government departments. Even if full-pay and benefits need to be given to the people in the system, it is still a worthwhile exercise for the economy.

- Existing investments in other tax systems like GST (both in terms of time and infrastructure) might also become redundant, but again that’s a one-time write-off, and minor as compared to the benefits the economy would reap.

- The proposal seems to imply that the components which would go to the states and local governments would be based on the location of the bank deducting the BTT. This would be wholly inappropriate as well as unfair, as revenues could get monopolized by large states and cities. A proper and fair distribution mechanism needs to be developed by the Planning Commission, as to what proportion of the 0.6% nationally would go to which state, and likewise for local governments. This would be difficult, especially in the case of local governments, but is not impossible.

- Although the proponents do not seem to think that a far-reaching tax reform like this would require constitutional amendments, one is not so sure. This needs to be studied in detail by relevant experts.

Conclusions:

- To use an over-used cliché, this is a genuine game-changer for the Indian economy and should be welcomed by tax-paying citizens as well as corporates.

- The overall benefits to the economy can be tremendous, if implemented well.

- This is going to bring about real and long-term changes and hence needs to be studied and publicly debated in detail.

- There seem to be many aspects of this proposal which have yet to be thought-through, which needs to be done expeditiously.

- Finally, this is one tax reform that the country and the economy need immediately and hence should be taken up as soon as possible.

PS: Full disclosure, large parts of the points mentioned above have been taken from the Arthakranti proposal, therefore full credit is due to them. I don’t make any claims of “original thought” on this. J

The writer works for a leading professional services firm

Get Swarajya in your inbox.

Magazine