Economy

Can The Latest GDP Numbers Be Blamed On Demonetisation And GST?

Karan Bhasin

Sep 09, 2020, 11:14 AM | Updated 11:13 AM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Ever since the growth numbers were released, there have been several statements that have been made by analysts, commentators, and political leaders regarding the state of the Indian economy.

Experts have opined that India’s economy has been underperforming — and many have used the recent economic contraction as evidence of the negative impact of demonetisation and Goods and Services Tax.

However, making such assertions is nothing short of lazy analysis — if not, no analysis.

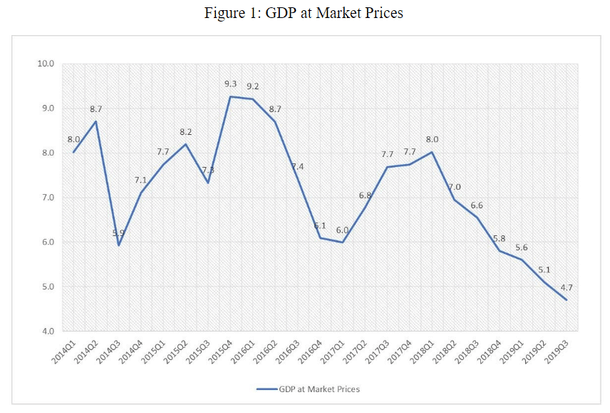

It is important to objectively look at how the economy has performed over the years before one arrives at any such conclusion (refer to figure 1).

The underlying data conclusively shows that the growth slowdown experienced in 2016 preceded demonetisation — there was a reduction in growth rate from 8.7 per cent in the first quarter to 6.1 in the third quarter.

There was some impact of demonetisation; however, the impact dissipates over time. This is consistent with several other studies, including Chodrow-Reich et al (2019), which highlight the short-run impact of demonetisation.

The next question is of Goods and Services Tax, which too had a slight positive impact in the immediately few succeeding quarters.

The question that thus emerges is whether the growth slowdown witnessed from 2018Q1 onwards was a delayed response to the reforms or are there several other factors that are also at play here.

The interesting part here is that when the Indian economy registered a growth rate of 8 per cent in 2018Q1, several members of the Monetary Policy Committee thought that the economy was overheating and subsequently, we saw several interest rate hikes.

This came at a time when the economy just went through two major reforms and needed an accommodative policy stance to help adjust to the new normal.

Moreover, we were dealing with financial sector stress due to a rise in Non-Performing Assets, which led to a problematic situation for our financial system.

The two rate hikes were aimed at preventing the economy from overheating and to ward off any inflationary pressures that could emerge over the coming few months.

While inflation continued to be non-existent, our real policy rates shot up substantially (refer to figure 2).

In fact, for a major part of the previous MPC’s tenure, the real rates have been higher than the target, pointing at the extent of monetary tightness that has been the norm since 2016 when the MPC took over.

This issue has been raised several times by me in the past, and more recently, Pramit Bhattacharya, Nikita Kwatra and Sriharsha Devulapalli made a similar argument.

Pramit et al blame bad data for this fiasco; however, that would be more dangerous as it would cast a serious doubt on the ability of the central bank to gather enough reliable quality statistics to formulate monetary policy.

What we do know, for sure, is that RBI’s Inflation Expectation Survey is of little value and relying on it is likely to create several policy blunders.

The question that, thus, emerges is, whether inflation and inflation expectations can be divorced?

But here is what we do know for a fact. In September of 2018, IL&FS collapsed and that triggered a major financial crisis in the Non-Banking Financial Sector.

Credit availability became a serious problem and subsequently, our growth started to falter.

In 2018 Q1, we were growing at 8 per cent — this was before the rate hikes. In 2019 Q3, our growth had slowed to 4.7 per cent. Then, Coronavirus started, and things got far too complicated with a public health emergency necessitating a lockdown to upgrade our healthcare infrastructure.

The fundamental point here is that it is unfair to blame the reforms for the growth recession that we witnessed from 2018 onwards.

Fact remains that our monetary policy was a major disaster as we had one of the highest real rates in the world — and as cost of capital went up, high amounts of leverage (borrowings) had an impact on balance sheets of corporates and NBFCs.

This is precisely why there is a genuine need to recognise just how important monetary policy is for the purpose of economic growth and consequently, development.

A more nuanced discussion of the same is needed — especially in the public discourse — to better recognise how these decisions have a direct impact on our lives.

While there have been several rate cuts since the new Governor took oath, transmission of these rate cuts to bank lending rates takes time.

These rate cuts have coincided with a slight uptick in inflation due to temporary supply disruptions which have pushed real rates as negative.

This is important during the pandemic and even afterwards to allow for corporate balance sheets to recover before we start pulling back on policy support.

The need to stress this arises from the fact that the previous MPC has indeed been hawkish and has been too concerned with inflation — even when it did not exist — and kept the rates higher than what was needed.

An increase in rates now would be a definite disaster and one hopes that the new MPC won’t undertake any such misadventure.

It is convenient to draw conclusions and paint the economic experience of the previous tenure of the present government using the last few quarters — but reality is that our growth experience was particularly good in 2014, 2015 and even first half of 2016.

This, despite two successive droughts in 2014 and 2015. Growth recovered and was decent even in 2017 or the first quarter of 2018 post which we saw two successive rate hikes.

There is a definite need to recognise just how important the conventional macro-policy tools are, be it fiscal or monetary policy and align these both with our growth ambitions to prevent as much scarring of the economy due to the pandemic as possible.

Get Swarajya in your inbox.

Magazine