Economy

External Borrowings And Debt Crisis: Should We Be Worried?

Karan Bhasin

Jul 09, 2019, 01:19 PM | Updated 01:19 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

The previous article highlighted potential reasons behind the government’s decision to look at external borrowings as a source of finance. The tricky part of the idea was to look at US$-denominated bonds rather than rupee-denominated bonds.

It is important to understand the East Asian financial crisis during the late 1990s and then contrast it with India in 2019. Such an exercise will itself make it apparent why we shouldn’t be worried about an external debt crisis.

Before we discuss the East Asian crisis, it is important to understand a few identities of international economics in the box below. You may skip the box and proceed directly to the main article.

East Asian Miracle And The Subsequent Crisis

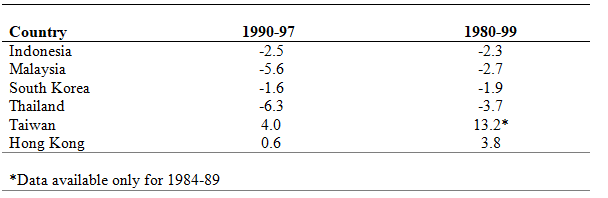

Since the 1960s several East Asian economies witnessed an acceleration in their growth rates due to a switch from the earlier import substitution policies of the government. In the 1970s and 1980s countries such as China, Malaysia, Thailand and Indonesia became a part of the high-growth Asian economies.

A common feature amongst these countries was a high rate of savings that were used to finance domestic investments. In the 1990s this trend changed as countries started to finance their investments through foreign investments and they started maintaining current account deficits (Refer to Table 1).

The Asian Financial Crisis started primarily because of prolonged macroeconomic imbalances due to the fixed exchange rate regime.

The Government of Thailand attempted a controlled devaluation of their currency, Thai Baht, in 1997. The controlled devaluation wasn’t successful and speculation led to a substantial capital flight that worsened the situation. With the sharp decline in Thailand’s currency, investor confidence in the emerging markets eroded and the crisis spread to other countries.

The situation was complex as most of these countries were net oil importers and they were heavily dependent upon trade for their growth. Therefore, a simple devaluation would have induced inflation, and with domestic debt denominated in US dollars, their liability would sharply increase.

The other alternative was to offer higher rates of interest to investors in order to curtail capital flight. The depreciation of currency led to a revival of exports and growth returned to normal in 1999, indicating a V-shaped recovery.

Towards A New India — With Sarkari US$ Bonds

It is evident that the East Asian debt crisis was largely driven by macroeconomic imbalances that resulted in capital flight. Subsequent and sharp devaluation of the currency deepened the crisis by spreading it across different sectors of the economies.

Therefore, the concerns with the use of dollar-denominated bonds are more to do with dollar-rupee valuations and the impact of a sharp devaluation of our currency on our foreign debt obligations.

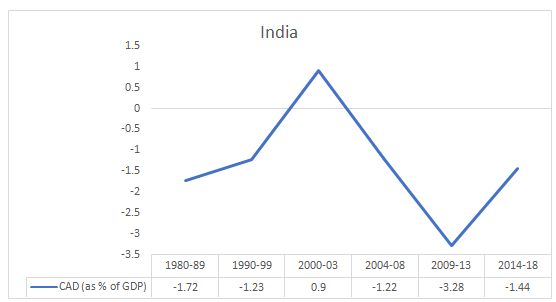

In the context of India, three important things are worth considering. First, our current account deficit is relatively moderate compared to the East Asian countries before the crisis. Second, our debt to GDP ratio and fiscal deficit both have been falling over the last five years. Third, our external sector borrowings are significantly smaller than most countries. In fact, our external sector borrowings are one of the lowest in the world.

Therefore, taking on additional external debt in a foreign currency is unlikely to create a debt crisis in the event of exchange rate volatility.

But will there be such volatility in our exchange rates to cause such a crisis? Not really. Especially because we don’t have a fixed exchange rate system and therefore, our exchange rate value is reflective of the prevalent macroeconomic situation. Therefore, any macroeconomic imbalance will be reflected in our exchange rates, which will give our policymakers a signal to formulate necessary policies to rectify the situation.

Additionally, with the FRBM (Fiscal Responsibility and Budget Management) Act in place, we’ve the necessary safeguards and frameworks to ensure macroeconomic stability over the medium term. This follows from the fact that we’ve largely been on the fiscal consolidation path over the last five years. Consequentially, our debt to GDP ratio has also fallen, and combined with low inflation, it demonstrates the strength of our fundamentals.

Stable and strong macroeconomic fundamentals are not just critical towards ensuring a stable exchange rate but they also impact our sovereign ratings, which in turn determine our ability to borrow at lower rates. Concerns of capital flight too are perhaps over-exaggerated, as even in the event of any changes in the US’s monetary policy, India’s central bank will appropriately change our monetary stance.

No matter how you look at it, the gains from sovereign US$ bonds are far too high while the risk is way too low. Therefore, if we just stick to our fundamentals and frameworks, we’re good to go!

Get Swarajya in your inbox.

Magazine