Economy

India In The World Economy — Its Rise After A Thousand Years Of Decline

Sanjeev Sanyal

Apr 29, 2024, 12:31 PM | Updated Aug 06, 2024, 12:31 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

India’s nominal GDP is set to hit USD 4 trillion in 2024-25. With Japan’s economy now valued at USD 4.1 trillion — reflecting a sharply weaker JPY — India is now tantalisingly close to becoming the world’s fourth-largest economy in dollar terms within a year.

Germany’s nominal GDP is valued at USD 4.6 trillion and is growing relatively slowly. So, it is now reasonable to expect India to replace Germany as the world’s third-largest economy by 2026-27. All of these projections are based on the assumption that no unexpected shock impacts the calculations, with the threshold levels indicating that it will now take a very big hit to significantly throw off the trajectory.

Of course, even as the world’s third-largest economy, India will still be poor in per capita terms but sheer bulk does provide advantages that can be leveraged. While we celebrate India’s economic rise, it should be remembered that India was a major economic power for much of history. Therefore, it is worth revisiting the longer cycle in order to appreciate what we are currently witnessing.

According to Angus Maddison’s widely used estimates, India accounted for around 33 per cent of the world economy in 1 AD. In order to avoid the vagaries of exchange rates and relative prices, these estimates were done on a purchasing power parity (PPP) basis. At that time China’s share at 26 per cent was the second largest while Western Europe, much of it under Roman rule, accounted for almost 11 per cent.

Obviously, these are rough estimates given the long expanse of time, but it is remarkable how India’s economy was such a dominant force two thousand years ago. Indian merchants were operating from the Middle East to East Asia, and Roman policy-makers were complaining about the current account deficit with India.

A thousand years later, India was still the world’s largest with a share of 29 per cent in 1000 AD. China’s share too had declined a tad to 23 per cent but was still the second-largest economy. Europe’s share had fallen below 9 per cent after the decline of the Roman empire. Africa’s economy, led by the Fatimids of Egypt, accounted for 12 per cent of the world economy; a share that Africa has not enjoyed before or since.

The global economy was dominated by supply chains running from the Fatimid Empire in Egypt to the Chola Empire in India, through to the Song Empire in China. Funded by temple banks, India’s merchant guilds created a vast trading network across the Indian Ocean and beyond. The Cholas would make two raids on Southeast Asia to keep the shipping lanes open in 1017 and 1025.

Turko-Mongol invasions and plagues in the thirteenth and fourteenth centuries cause serious damage to all the major economic nodes. By 1500, China had recovered under the Ming Empire to become the world’s largest economy with a share of 25 per cent. India’s share had by now declined to 24.5 per cent but, with the Vijayanagar empire at its height, it was still the second largest.

By 1600, however, China’s share jumped to 29 per cent. In contrast, India’s share dropped further to 22.6 per cent as the economic shock of the sacking of Vijayanagar, then the world’s largest city, was not compensated by the establishment of the Mughal empire. The Mughals nurtured some economic hubs but disrupted others as a part of their conquests.

Importantly, the impact of the Renaissance and overseas maritime discoveries pushed the share of Western Europe to 20 per cent by 1600. Italy and France dominated the European economy at this stage. Surprisingly, Spain and Portugal remained relatively small economies despite their global empires. The cost of managing this empire and incessant wars used up the silver and gold shipped in from the Americas.

The subsequent centuries saw the expansion of European colonisation and, from the late eighteenth century, the Industrial Revolution. However, China remained the world’s economic superpower. In 1820, China accounted for 33 per cent of global GDP while India’s share had dropped to 16 per cent. Colonial exploitation by the East India Company and the incessant wars with Marathas (and others) had taken their toll.

Commentators often state that China and India together accounted for half the world economy in 1820 but note that China accounted for twice as much as India at this stage. Western Europe’s share amounted to 23.6 per cent — Britain’s at 5.2 per cent and France’s at 5.5 per cent (so the French economy was still a little bigger despite the loss at Waterloo).

The nineteenth century was a time of very radical shifts. China’s share dropped to 17 per cent by 1870 and then to 9 per cent by 1913. India’s share similarly dropped to 12 per cent and then to below 8 per cent on the eve of the First World War. India’s place in the world clearly suffered from the colonial occupation but notice that China’s decline was even more dramatic. The Opium Wars, the various internal rebellions and technological stagnation took their toll.

In contrast, the share of Western Europe rose to peak at 33.5 per cent of the world economy between 1870 and 1913. The relative trajectories of individual countries, however, are interesting. Britain’s share rose to a peak of 9.1 per cent in 1870 and then declined to 8.3 per cent (this excludes its colonies). That of Germany rose from 6.5 per cent to 8.8 per cent in the same period. Thus, Germany had a larger economy on the eve of the First World War but Britain had an empire.

Meanwhile, the United States had grown very rapidly over the previous century to become the world’s single-largest economy with a share of 19 per cent in 1913. Following the Second World War, its share rose to over 27 per cent by 1950. The USSR with a share of 9.6 per cent was a distant second (this would be its peak and it would gradually decline over the next four decades till it finally collapsed).

Exhausted by the two wars and the steady loss of its colonies, Britain’s share had declined to 6.5 per cent by 1950 and the number has continued to decline ever since. The shares of newly independent India and China were similar at 4.2 per cent and 4.5 per cent respectively. This was a drastic loss for the two civilisations that had dominated the world economy for millennia, but the Chinese perhaps felt the humiliation more keenly as the decline had happened more recently and sharply.

Perhaps the most dramatic shift of the next quarter century was the rise of Japan. It had accounted for just 3 per cent of the world economy in 1950 but accounted for 7.7 per cent by 1973 when the first oil shock hit the world economy. Also interesting is the fact that India’s place in the world economy continued to slide despite independence, and Nehruvian socialism would pull down its share to 3 per cent by the early seventies. Economic freedoms matter just as much as political freedom.

From here we will switch to IMF estimates. These are in the same ballpark as those of Maddison but can be extended to the present day (Maddison’s estimates end in 1998).

In 1980, the US was still the world’s dominant economy with a share of over 21 per cent of world GDP. India’s share was just 3 per cent and China, after all the chaos of the Cultural Revolution and the Great Leap was down at 2.3 per cent. Both economies began to reform from here — China more systematically, and India initially tentatively till it became more serious after the crisis of 1991.

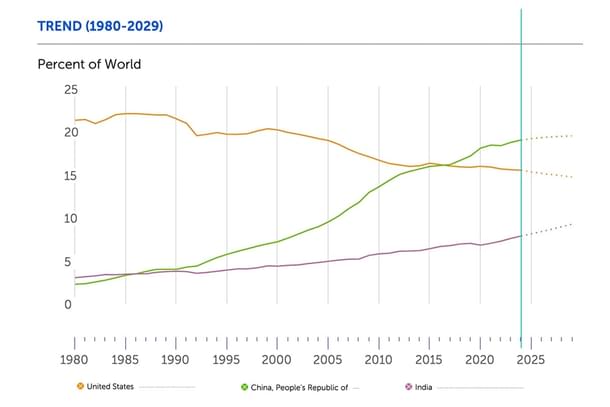

Improved policies led to improved performance. China’s share jumped to 7.2 per cent by 2000 and by 2017 it equalled the US’ share of 16 per cent. At the time of writing in 2024, it now accounts for 19.4 per cent of the global economy and is again the world’s largest economy.

The US is still the world’s largest economy in nominal dollar terms but in PPP terms its share is now down to 15.5 per cent. Meanwhile, India’s share has been rising steadily. It rose from 4.3 per cent in 2000 to almost 8 per cent in 2024. In other words, it is already the world’s third-largest economy in PPP terms. Recall that this was India’s share on the eve of the First World War, and still far below its pre-colonial share.

The IMF predicts that by the end of this decade, China’s share of the world economy in PPP terms will level off at 19.5 per cent while that of the US will decline further to 14.7 per cent. Japan’s share will come down to 3.2 per cent while that of Britain will be at 2 per cent.

In contrast, India’s share is expected to rise to 9.2 per cent of the world economy by 2030. This is no small reversal in fortune for an economy that has suffered such a long cycle of relative decline.

Indeed, the importance of India’s current rise can only be properly understood on a civilisational timescale. While we rightfully celebrate the recent turn of fortune, it is also important to remember that we have a long way to go before India recovers its historical place in the world.

References:

- The World Economy: A Millennial Perspective, Angus Maddison, OECD 2001

- IMF Datamapper, World Economic Outlook, April 2024

- The Ocean of Churn, Sanjeev Sanyal, Penguin 2016

(The author is an economist and bestselling writer. All opinions are personal).

Get Swarajya in your inbox.

Magazine