Magazine

Will 2019 Be A 1929? All The Elements Of A Volatile Cauldron Are In Place

Shanmuganathan Nagasundaram

Jan 01, 2019, 04:19 PM | Updated 04:19 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

The year 1929 was the beginning of what is now known as the Great Depression — a period of prolonged economic stagnation worldwide that was triggered by the American stock market crash of October 1928. Between 1929 and 1933, the global gross domestic product (GDP) had plunged by 15 per cent and the economic stagnation continued till 1940 — or until 1946 — depending on how we choose to view GDP itself. Bulk of the addition to the GDP post 1940 was wartime goods production, which neither had a market pricing nor any consumer utility. Most objective measurements showed a declining standard of living until 1946.

As I see it, we are set for a repeat of the Great Depression — worse in many ways as I will explain — in the years ahead. Whether it starts in 2019 or a bit later is something that is hard to predict, but all the ingredients of a volatile cauldron are already in place. An extraordinarily lax monetary policy for more than a decade — especially in the US, Europe and Japan, simultaneous bubbles in a variety of asset classes (equities, bonds and real estate), untenable public and private leverage within the system, government spending that is simply out of control worldwide and a generally clueless population about the prosperity foundational axioms of individual liberty, limited government and sound money.

Over the course of this article, I am drawing upon the teachings of Adam Smith, Von Mises and Murray Rothbard. Their writings on free markets and its invisible hand, economic/business cycles, interest rates and central banking form the backbone of Austrian economics and that’s what I have used to draw my inferences.

Recession 101

Let me start with what a recession is as that’s one of the most misunderstood topics in economics. A recession is a cure to the malinvestments made during an economic boom, to redirect resources to the parts of the economy, where it is needed and away from the overheated/bubble sectors. While booms and busts are inherent in almost all economic activity, the frequency as well as the amplitude are accentuated by the effects of central banking and cheap money.

There is usually a multiplicity of factors that is associated with the formation of bubbles. But the one necessary and, perhaps, even sufficient condition is loose monetary policy. The rest are just the bells and whistles. The common thread behind the seemingly disparate bubbles — the 2000 Nasdaq bubble, 2008 housing bubble, and the 2019/20 ‘currency bubble’ (we will get to this later) — is a loose monetary policy.

The bubbles also tend to get bigger with time just on account of the increased amount of money and credit circulating within the system. Consequently, the inevitable bursts also tend to be more devastating in its consequences. Perhaps, much more importantly, the so-called corrective actions taken by central banks to mitigate the effects of the bubble burst lay the foundation of the next bubble. So the Nasdaq 2000 bubble burst and ‘the maestro’ Alan Greenspan leaving interest rates at 1 per cent for a few years pretty much caused the 2008 housing bubble. If a few years of 1 per cent interest rates could cause the 2008 crisis, just imagine what nearly a decade of ZIRP (zero interest rate policy) and QE (quantitative easing) are going to cause when the current all-but-commodities bubble bursts. The year 2008 is going to look like the proverbial Sunday school picnic.

What should the government really do in a recession? Actually nothing. Just allow the malinvestments to be liquidated in the markets. As Andrew Mellon, the treasury secretary during 1929 advised “liquidate labour, liquidate stocks, liquidate the farmers, liquidate real estate. It will purge the rottenness out of the system”. Needless to add, it was completely ignored by the then supposedly ‘free markets’ oriented Herbert Hoover.

The only legitimate actions that a government should undertake during recessions would be to deregulate, cut taxes and reduce government spending to free up capital for private investments. A good historical account of such a laissez faire approach and the results thereof can be understood from Jim Grant’s The Forgotten Depression: 1921: The Crash That Cured Itself.

The current solution of a fiscal stimulus is pure ‘Keynesian snake oil’ that just postpones the day of reckoning while compounding the problems at the same time. A good metaphor that can be used to understand recession is that of a drug addict on an artificial high and the withdrawal symptoms while trying to quit the habit. The equivalent of the drug is the central bank sponsored cheap money, the highs are the asset price booms and the withdrawal symptoms are the equivalent of a market induced recession. It’s just a necessary cure to clear the system.

What Caused The Great Depression?

Most of what is popularly believed about the causes of the Great Depression is just plainly wrong. In fact, they are deliberately falsified versions of economic history for governments to absolve themselves of the blame and provide a justification to usurp greater powers. Interested readers can read the Murray Rothbard classic America’s Great Depression to understand the details.

Summarising the propaganda, it is that the stock market crash of October 1928 was a normal business cycle downturn. What made the downturn a prolonged major depression was a passive/deflationary monetary policy and a laissez faire attitude of the Herbert Hoover government. As Ben Bernanke summarised in a 2002 lecture in honour of Milton Friedman “Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again”. There’s remarkable agreement amongst the Keynesians and the Monetarists on this issue.

Am I saying that Bernanke is deliberately lying on the causes of the Great Depression? I wouldn’t be surprised if that were indeed to be the case. But, perhaps, a more systemic rationale for such explanations is that the economists, who are appointed to positions of power and influence are the ‘useful idiots’.

But as Rothbard explains, the truth is very different. The US Fed blew up a stock market bubble during the ‘roaring twenties’. When the bubble burst, as all bubbles eventually do, Hoover and later Franklin Roosevelt repeatedly intervened in the market with all kinds of actions including wage and price controls, the New Deal, confiscation of gold and destruction of output to artificially raise food prices.

The US Fed did indeed play a relatively passive role as they should have, but the depression was eventually blamed on the deflation. The economic truth, however, is that the deflation made the depression a lot more tolerable than would have been otherwise.

Since most people associate deflations with depressions, I should point out that the entire nineteenth century in which the US when it rose from a backward agrarian society to an industrial powerhouse was deflationary. The gold standard that produces one of the remarkable objectives of “growth with reducing inequalities” is deflationary, almost by definition.

The Crisis Ahead

The nature of the crisis that lies ahead for the US economy is quite unlike what we have witnessed in the last few decades — at least in a developed economy. The bubbles will burst — equity, bond and real estate — and there is some evidence that this process may already have begun in the last few weeks.

But what prevents the US Fed from undertaking another round of QEs and ZIRP to blow some air back into these bubbles? Perhaps just an increased quantity of QE should do the trick this time around.

Also, there doesn’t seem to be any major side effects to these QEs anyway in the form of inflation. Why can’t Jerome Powell do just what Donald Trump suggested and focus on growth?

Firstly, I have very little doubts that both the interest rates hikes as well as the current QT (quantitative tightening) programme will be reversed by the US Fed very soon. The first signs of recession should be obvious even to the Fed early next year, and by the middle of 2019, we should well be into the process of returning to ZIRP as well as QEs. But unlike the first rounds of QE, the effects on asset classes are going to be very different this time around. Why so?

As Jens O Parsson describes in his book, Dying of Money, “everyone loves an early inflation. The effects at the beginning of inflation are all good. There is steepened money expansion, rising government spending, increased government budget deficits, booming stock markets, and spectacular prosperity, all in the midst of temporary stable prices. Everyone benefits, and no one pays.”

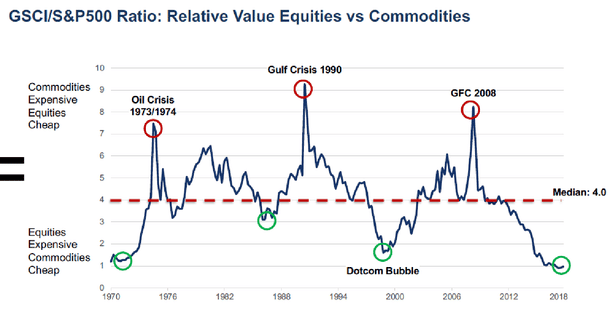

Which is pretty much what happened from 2008 to 2018. All of the inflation created by the central banks went directly into the good assets of equities, bonds and real estate. The result of the QEs and ZIRP was “one big, fat, ugly bubble” as candidate Trump correctly identified. As shown in the graph below the valuations of equities is so extreme that on a relative basis, commodities are cheaper today than in 1971.

So what happens next? Continuing with Parsson’s thesis on the inflationary cycles, “…the latter effects (of inflating the money supply) patiently wait. In the terminal inflation, there is faltering prosperity, tightness of money, falling stock prices, rising taxes, still larger government deficits, and still soaring money expansion, now accompanied by soaring prices and the ineffectiveness of all traditional remedies. Everyone pays and no one benefits.”

And that’s what will happen with QE4 to QE(N). A repeat of the 1970s stagflation (inflation combined with a recession) in which the traditional central bank remedies cease to work. A legitimate question at this stage would be that “if the problem is similar to the one during the 1970s, then why not the solution adopted during the 1970s?”

The reason is debt. The national debt of the US government was less than a $1 trillion in 1980 and most of it was financed through 30-year treasury bonds. This allowed the then Fed chairman Paul Volcker to hike the US Fed funds rate to 22 per cent to quell the inflation. That accumulated a national debt of $1 trillion, which took more than 100 years since the formation of the republic to reach, the US government now adds in a single calendar year.

Given that the current debt is in excess of $21 trillion and will increase at the rate of $1.5-$2 trillion a year (the Congressional Budget Office projections do not factor a recession for the next 10 years), even at 5 per cent interest rate, the US government finances would resemble that of Italy’s.

Also given that almost the entire debt is ARM’s (adjustable rate mortgages), the US economy doesn’t have the legs to afford ‘a Volcker’. This brings us to the currency bubble that I had alluded to early on in this article.

The End Game

“It costs only a few cents for the Bureau of Engraving and Printing to produce a $100 bill, but other countries had to pony up $100 of actual goods in order to obtain one” — Barry Eichengreen

The ability to issue currency is an enormous privilege and all central banks have abused that to varying degrees. The US Fed by virtue of the US dollar being the world’s reserve currency has had the opportunity to abuse that privilege the most. When the recession hits the US economy, and it’s very likely to do so in 2019, the choices in front of the US Fed would be quite stark:

a. Continue the path of hiking rates as well as QT, albeit at a subdued level.

b. Abandon the normalisation process and revert to ZIRP and QEs.

The above choices are on the monetary side. From the fiscal as well as regulatory side, we know that the political class will rely far less on the ‘invisible hand’ of the markets and much more on the heavy hand of the governments. There’s little doubt that Trump and ‘a Sanders’ (the most likely successor in the event of a recession in 2019) would make Hoover/Roosevelt look like laissez faire presidents by comparison.

If you think the current $1.5 trillion fiscal deficit under Trump is large, just wait for a few years and this number will look small in comparison.

The choices on the monetary side, however, will have much greater impact on the future course for the US dollar. If the US Fed continues path (a) — the tightening route — then a repeat of the Great Depression is on the cards.

Given the nature of imbalances and the virtual dismantling of the manufacturing sector in the US economy, the recession is likely to be worse than it was during the 1930s. But the silver lining would be that the US dollar will survive.

Make no mistake, quite unlike the 1930s, the US dollar will lose a substantial portion of its value vis-a-vis sound money, ie gold. But it will survive to fight another battle, another day.

But everything we have seen over the last few decades since the days of Volcker points to path (b). The remarkable consensus amongst the economists as to the cause of the Great Depression as well as the seeming success of ZIRP/QE as a response to 2008 (as pointed out earlier, all that ZIRP/QE 1, 2, 3 has managed to postpone the day of reckoning while making the causative problems of debt and leverage substantially bigger) does indeed guarantee QE4 to QE(N).

What this would lead is to make the other central banks question the currently undeserving status of the world’s reserve currency granted to the US dollar. It should (whether it does, I am not sure) also make the citizens of every country question the role of their individual central banks in debasing their individual currencies. One of the properties of money is a store of value and these fiat currencies have amply demonstrated over the last 100 plus years that they are anything but a store of value.

I am also sure that Trump would blame the US Fed for the recession and the subsequent collapse when it starts in 2019/2020. I am also sure that some of the ‘usual suspects’ would be the trade war with China, Trump’s tax cuts etc. But a legitimate search for an answer has to go back a lot in time. At the very least, to the days of Greenspan if not until 1971, when Nixon closed the gold window.

Personally, I would go back to 1913 as the source of the problem when the US transitioned from the classical gold standard to having a central bank that surreptitiously usurped the monetary function of the free markets. Once we crossed that rubicon, it’s a long slippery downhill slope, where the result is a guaranteed destruction of the currency. The US dollar might well be on its last incline of that slope.

Unfortunate and terrible as it sounds, it could get worse. There is just too much complacency within the system for anything worthwhile to be done before the collapse. But if we do recognise the underlying issues and return to a system of limited government, individual liberty and sound money, then the crisis would well be worth it. But my guess is that we will again end up pointing the finger at all the wrong directions — capitalism, greedy speculators, foreign mercenaries and the unregulated trading system.

The solutions then are likely to be the exact opposite of what’s needed and we might well have greater capital controls, higher taxes, more bureaucracy and more aggressive alpha males on top of the governance structure.

That would be the real unfortunate part and that’s the most likely outcome as well.

Shanmuganathan N (aka Shan) is an Economist based in India. He is the author of the recently published book "RIP U$D: 1971-202X …and the Way Forward" and can be contacted at shan@plus43capital.com

Get Swarajya in your inbox.

Magazine