Columns

Oil Prices - Has Putin been shown his place?

Jaideep A Prabhu

Dec 11, 2014, 05:52 PM | Updated Feb 10, 2016, 05:15 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Could it be that the recent drop in oil prices is a quasi-covert operation to sap the economies of the US and Saudi Arabia’s enemies? It is time that Vladimir Putin learn from the lessons of 1986 or 1998 to protect Russia’s interests.

One of the great barometers of the world economy, the price of oil, has been in steady decline over the past four months. From slightly above $115 dollars per barrel in June 2014, the price of black gold has fallen to a five-year low of below $66 in December 2014. It seems like just yesterday when analysts were talking about the possibility of oil prices breaching even $200 per barrel.

After all, oil was selling at $120 per barrel already, Fukushima had temporarily scared some countries off nuclear power, sanctions on Iran were cutting off their contribution to the global oil supply, war clouds were looming on the horizon in the Middle East as the war of words between Israel and Iran was heating up, and the spread of the Arab Spring into Syria and the descent of Libya into chaos further curtailed supplies. The second half of 2014 has gone against all expectations.

A few factors contributed to this 40+ per cent decline in oil prices. First, the world economy slowed down and major consumers like the European Union, Brazil, and China began to consume less oil; second, countries like Mexico and Canada expanded their oil production with new investments in offshore assets and tar sands extraction; third, the United States began to import less oil because of a shift to alternative energies as well as the development of shale oil; fourth, many countries began to shift some of their imports from crude oil to natural gas; fifth, Russia was able to boost its oil production despite sanctions against it by the West as the second stage of their Eastern Siberia-Pacific Ocean pipeline began operations; and sixth, countries like Libya, Iran, and Iraq have been able to increase their production despite the strife and instability in their countries.

Last week, a summit meeting of the Organisation of Petroleum Exporting Countries along with other oil exporting countries such as Russia and Mexico was held in Vienna. The twelve member countries — Algeria, Angola, Ecuador, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, the United Arab Emirates and Venezuela — discussed the falling oil prices and contemplated a cut in production to maintain prices around $90 per barrel.

However, no agreement could be reached and, instead, Saudi Arabia threatened a price war against American shale. For anyone not exposed to the oil industry, this bodes well. For example, India has finally started to make noises about economic reforms after five years of sluggish economic growth and the low price of hydrocarbons may be just the lubricant needed to hasten the results of those reforms.

The plummeting of oil prices and OPEC’s relative inability — or at least unwillingness — to stem the downward slide also reveals a new reality in the oil industry: OPEC no longer calls the shots on oil. With new players entering the market, OPEC’s total share of the international oil market has slipped to only 42 per cent and its influence correspondingly weakened.

Yet, why would Saudi Arabia want to get into a price war with US shale? The argument goes that if prices are low enough, Riyadh may force the shale oilmen out of business. For the House of Saud, this price war is not about earnings but about market share and it is willing to endure lower revenue in the short term. However, there are snags in this logic: if the price of oil were to fall to $40 and remain there for a while, it would certainly force some of the shale producers out of business, but some oilfields can still be profitable at that price and continue to function. Thus, Riyadh’s strategy would only partially be successful. More significantly, lower oil prices would presumably increase demand, and that would nudge the prices upwards again and make more shale profitable. The Saudi game is costly, risky, and painful to sustain over even a medium period of time.

An even more intriguing wrinkle in Riyadh’s willingness to bear the difficulty of lower oil prices is that the kingdom has, along with other Persian Gulf oil economies, invested heavily in social sector spending. In order to stave off the spread of the Arab Spring, the Gulf oil economies embarked on massive infrastructure development projects and increased subsidies substantially.

Lower oil prices would mean that these states will not be able to balance their expanded budgets. According to the International Monetary Fund, most of these economies need the price of oil to be well over $100 per barrel. Refusing to cut production and engaging in a price war that may well see oil prices fall to $40 per barrel makes little sense, and the shortfall of $60 per barrel is not a mere inconvenience but a body blow to their economies. Admittedly, most of the Gulf states have strong financial assets, but the slower world economy has not been too kind on those either. However, some level of mitigation is found in the Gulf’s pegging its currencies to the dollar: the US Federal Reserve has a strong influence on Gulf monetary policy and, therefore, Gulf currencies move along with the dollar. The strengthening dollar over the past six months has also made the Gulf’s imports cheaper.

Saudi Arabia’s strange moves all add up to one possibility that Thomas Friedman of The New York Times and Paul Richter of The Los Angeles Times alluded to last month: the US and Saudi Arabia are waging a secret war against their enemies through oil prices. At first glance, this may seem utter nonsense given the burden on Riyadh itself, but the countries likely to be hurt the most — Russia, Iran, and Venezuela — are all antagonistic to the US. Saudi Arabia also has a keen interest in debilitating Iran in the region as well as individually, and Russia has proven to be a hindrance to Saudi interests in Syria.

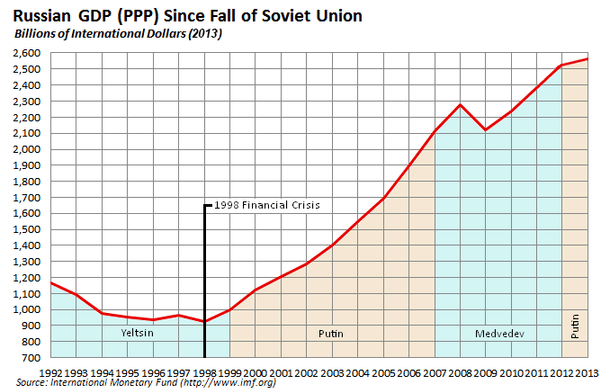

The idea of a quasi-covert operation to sap the economies of the US and Saudi Arabia’s enemies is not at all far-fetched. In 1986, at the height of US-Saudi involvement in Afghanistan against the Soviet Union, President Ronald Reagan leaned on his Gulf ally to turn on the oil tap in an effort to hamstring the Soviet economy. Reagan’s policies were based also on domestic energy price considerations and the Soviets sold much of their oil at fixed prices to their Warsaw Pact clients, but the net effect was the same: a shrinking of Soviet oil revenues and a run on the rouble.

In 2014, it is calculated that lower oil prices would exert pressure on Tehran to negotiate in earnest over its nuclear programme; it will also reduce funds available for Iranian misadventures in Syria, Iraq and Lebanon. This is to the benefit of the US, Saudi Arabia, and Israel. Similarly, lower oil prices would make the sanctions against Russia due to the Ukraine crisis bite more; it would be harder for Moscow to woo China and India, the Russian military modernisation programme will have to take a break, and Russia’s ability to meddle in Syria would be restricted. Again, this is all to the benefit of the US and its allies.

An important piece in this geopolitical jigsaw is the US ban on the export of oil. Keeping US shale off the international market reduces competition to Riyadh’s advantage. From a purely economic point of view, it would be in Washington’s interests to lift the ban and capture market share as well as sizeable revenue. It is difficult not to wonder if there is not a secret agreement between the oil sheikhs and Foggy Bottom to maintain low oil prices for a period of time in exchange for Washington DC staying the ban on its oil exports to give the Gulf the opportunity to make up in volume for its losses in capital.

Of course, the impact of lower oil prices might be mitigated through various mechanisms like barter. There have already been some noises from Tehran and Russia about trade in local currencies and barter of essential commodities. Russia may even take out its frustration with the West on the nuclear talks with Iran or step up its weapons sales to less savoury clients. This may stave off the worst but is not a solution for the long term.

If the US has indeed orchestrated this drop in oil prices, it is the first intelligent and aggressive move by Obama’s White House. It is surprising that Vladimir Putin, the suave, realpolitik, ex-Soviet intelligence officer, did not learn from the lessons of 1986 or 1998 and left Russia vulnerable to fluctuations in oil prices. Fun as it is to speculate on the causes of the ‘oil holiday’, countries like India will make hay while the sun shines.

Jaideep A. Prabhu is a specialist in foreign and nuclear policy; he also pokes his nose in energy and defence related matters.

Get Swarajya in your inbox.

Magazine