Economy

Decoding GDP 2020-21

TV Mohandas Pai and Nisha Holla

Jul 24, 2021, 03:27 PM | Updated 03:27 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

India's Central Statistics Office recently released provisional estimates for national Gross Domestic Product (GDP) and income for the fiscal year 2020-21.

The composition and quarterly trends of GDP last year is of national interest to gauge the impact of the Covid-19-pandemic on the economy. Moreover, decoding this data is also helpful for focusing on the next economic stimulus package to drive growth in FY'22.

In the wake of the pandemic, most analysts opined that the Indian economy would contract by 8-10 per cent in real terms because of the total lockdown in FY'21 Q1 and partial in Q2.

However, as growth picked up in Q2, some of them had revised it upwards to a decline of 7.5 per cent. The provisional estimates show a contraction of 7.3 per cent — from Rs 145.7 lakh crore real GDP in FY'20 to Rs 135.1 lakh crore in FY'21.

In nominal terms, GDP declined from Rs 203.5 lakh crore in FY'20 to Rs 197.5 lakh crore in FY'21 — a contraction of 3 per cent.

Per-capita nominal GDP plunged by 4 per cent, from Rs 1.52 lakh in FY'20 to Rs 1.46 lakh in FY'21.

Analyzing the budget in nominal terms gives a better indication of what transpired since it reflects the prices people experience and transact with today.

A close look at the breakdown of nominal GDP highlights changes in three essential components:

Private final consumption expenditure (PFCE) declined from Rs 123.1 lakh crore (at 60.5 per cent of GDP) in FY'20 to Rs 115.7 lakh crore (at 58.6 per cent of GDP) in FY'21. As consumption reduced due to the lockdown in FY'21, there is an Rs 7.4 lakh crore drop in PFCE. This decline is crucial as growth in the Indian economy depends heavily on internal consumption.

Government final consumption expenditure (GFCE) increased from Rs 22.9 lakh crore (at 11.2 per cent of GDP) in FY'20 to Rs 24.7 lakh crore (at 12.5 per cent of GDP) in FY'21. This amounts to an increase of Rs 1.8 lakh crore — less than the Rs 2.5 lakh crore increase between FY'19 and FY'20. The precise impact of (higher) government spending in FY'21 needs examination.

Gross fixed capital formation (GFCF), representing the aggregate capital investment in the country, also declined from Rs 58.5 lakh crore (at 28.8 per cent of GDP) in FY'20 to Rs 53.5 lakh crore (at 27.1 per cent of GDP) in FY'21.

Both private consumption and capital investment declined in FY'21 due to the economic activity shutdown in the first two quarters.

Breakdown by sector

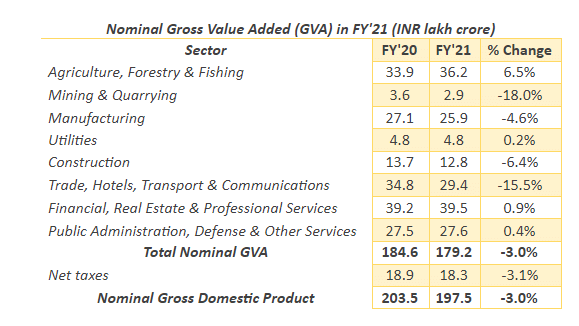

GDP is the sum of the Gross Value Added (GVA) and net taxes on products. A closer look at the nominal GVA composition in Table 1 reveals which sectors were most affected by the pandemic-induced lockdown in FY'21. Agriculture is the only sector that recorded positive growth of 6.5 per cent, increasing from Rs 33.9 lakh crore in FY'20 to Rs 36.2 lakh crore in FY'21. This is a direct result of not shutting the rural economy during the first wave and enabling farmers to harvest the record high rabi crop, sow and harvest the kharif crop, and benefit from various schemes, including PM-KISAN.

Manufacturing declined by 4.6 per cent, from Rs 27.1 lakh crore in FY'20 to Rs 25.9 lakh crore — a direct consequence of the lockdown that prevented factories from staying open and a dramatic reduction in trade.

Construction dropped by 6.4 per cent, from Rs 13.7 lakh crore in FY'20 to Rs 12.8 lakh crore in FY'21, reducing job availability leading to higher unemployment.

The pandemic also directly affected the retail, hospitality and travel industries, and this is evident in the steep decline of 15.5 per cent in the GVA of the services sub-sector consisting of Trade, Hotels, Transport and Communications — from Rs 34.8 lakh crore in FY'20 to Rs 29.4 lakh crore in FY'21.

This services sub-sector was a major casualty of the lockdowns, leading to large-scale job losses; it is yet to recover.

Another significant services sub-sector is Financial, Real Estate and Professional Services that grew marginally by 1 per cent — important to note because usually this sub-sector grows at 7+ per cent and the difference of 6+ per cent growth is a significant loss to economic growth.

Lastly, net taxes declined by only 3 per cent, indicating the taxpaying sector was not unduly affected by the pandemic and lockdown.

Quarterly growth

Analysis of quarterly nominal GDP growth clearly shows the Indian economy was gaining traction after the lockdown in Q1 and partially in Q2 in FY'20.

Table 2 shows GDP quarter by quarter over the last three years. The FY'20 Q1 grew at 9.6 per cent over FY'19 Q1, the highest growth percentage change compared to the other three quarters — indicating that FY'21 Q1 might have also accelerated.

But, instead, because of the pandemic and a national shutdown of the economy, FY'21 Q1 recorded a decline of 22.3 per cent over FY'20 Q1.

The economic decline slowed down significantly in Q2, at -4.4 per cent compared to FY'20 Q2, as the lockdowns eased and businesses and manufacturing came back online.

As a result, FY'21 Q3 went into full swing, recording growth of 5.2 per cent over FY'20 Q3 — considerably close to the 6.5 per cent FY'20 Q3 recorded over FY'19 Q3.

The momentum enabled FY'21 Q4 to catch up to 8.7 per cent over FY'20 Q4 — same as the percentage change of FY'20 Q4 over FY'19 Q4.

The year-end momentum is corroborated by the all-time high GST collections of Rs 1.41 lakh crore in April 2021 for sales in March 2021. Similarly, the corporate sector, which saw a decline in revenues in FY'21 Q1, recovered rapidly to record all-time high profits in Q2, yet again in Q3 and exceeded again in Q4.

The Indian economy was coming back on track towards the second half of FY'21, and robust estimates were made for economic growth in FY'22.

Real GDP growth estimates were in the range of 10-12.5 per cent, translating to 14-16.5 per cent in nominal terms to include inflation. However, due to the second Covid-19 wave and resultant state-wise lockdowns, FY'22 Q1 will again record a down quarter, and Q2 will see some recovery with the gradual unlocking across India.

Growth estimates have now downshifted to 7.5-10 per cent.

India needs a fiscal stimulus

The quarterly GDP estimates, sectoral GVA breakdown and trends in consumption and capital investment clearly show the major levers of the Indian economy.

By focusing on these levers, it is possible to meet the high growth requirement of FY'22 with substantial job creation to counteract the large-scale employment loss caused by the pandemic.

However, this rests a great deal on an imminent economic stimulus by the government that incentivizes consumption, manufacturing, construction and extensive job creation.

A monetary stimulus will no longer be effective; a fiscal package is the only way to ensure FY'22 records healthy growth. The Indian economy is robust and has proven it can rebound from a couple of down quarters like it did in FY'21.

All it needs is a strategically directed boost to recover faster and stronger in FY'22.

TV Mohandas Pai is Chairman, 3one4 Capital, and Nisha Holla is Research Fellow, 3one4 Capital

Get Swarajya in your inbox.

Magazine