Economy

Is Rajan Trying Too Hard To Prove His Rate Strategy Worked? He Should Relax

R Jagannathan

Jul 27, 2016, 03:33 PM | Updated 03:33 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Outgoing Reserve Bank Governor Raghuram Rajan seems keen to prove that he did a good job as India’s chief moneyman. Yesterday (26 July), speaking at the 10th Statistics Day Conference, he tried to suggest once more that inflation was down largely because of his actions.

He made four points: that growth was not being throttled by his interest rate policy; that the sharp drop in oil prices was not the main reason for inflation coming down; three, the deceleration in credit growth was not due to high cost credit; and four, the RBI had a large hand in bringing inflation down.

He backed his first argument by pointing out that India cannot claim both to be the fastest growing economy in the world and yet that growth is being killed by high rates. But, by the same token, Rajan too has contradicted himself; he has doubted the high GDP figures and yet defended his rate policy.

But he is right to say that it is not rates that are killing growth. It is corporate indebtedness.

He also disproved claims that high rates and/or shortage of capital were restricting demand for credit. Private sector banks, for example, are showing high credit growth. Even public sector banks are showing growth in retail credit. But they were reluctant to lend to large corporates and large projects. Rajan concludes: “In sum, the Indian evidence…suggests that what we are seeing is classic behaviour by a banking system with balance-sheet problems. We are able to identify the effects because parts of our banking system do not suffer from such problems. The obvious remedy to anyone with an open mind would be to tackle the source of the problem – to clean the balance-sheets of public sector banks, a remedy that has worked well in other countries where it has been implemented. Clean up is part of the solution, not the problem, and that is what we are doing.”

It is the last point – how much credit to assign to monetary policy for the drop in inflation – that is debatable. While admitting that falling fuel prices played their part in bringing down inflation, Rajan claims a large role for monetary policy in this fall. He offers three arguments to prove his point.

First, the high interest rate policy pre-dated the fall in fuel prices, which happened in 2013 and 2014 respectively. This is right.

Second, the fuel price fall was not fully passed on to consumers, with government raising excise duties. While crude prices fell 72 percent between August 2014 and January 2016, petrol prices fell only 17 percent. So the actual fuel price cut was not as significant as imagined. Ergo, they were a marginal factor in the inflation drop.

Here, Rajan is only partially correct, for some other fuel prices fell dramatically, especially non-subsidised LPG. The price of non-subsidised LPG fell from nearly Rs 1,241 per 14.2 kg cylinder in early 2014 to around Rs 548 now (in Delhi). So the average cut in fuel prices was actually more than the petrol price cut shows. By using only petrol data, Rajan was a trifle misleading on this point.

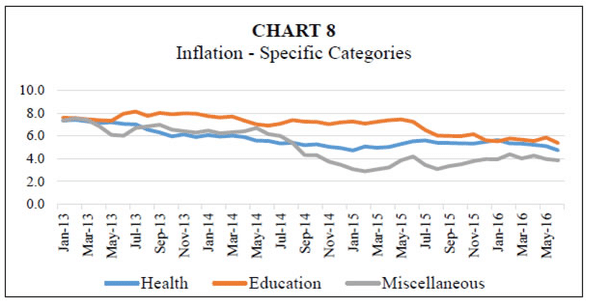

Third, Rajan refers to falling inflation in non-food, non-fuel, non-traded products to prove the efficacy of his rate strategy. Inflation in the health and education sectors too came down – two sectors that had little to do with fuel price changes (see chart)

But can the downtrend in health and education be put down to his rate policy? The fact is, by the third quarter of 2013, when Rajan joined the Reserve Bank, the economy was already decelerating. Rural wages were falling, and growth and incomes were slowing. The government was slashing capital investment to meet fiscal targets. High inflation in essentials was also eating into discretionary spends, thus impacting demand in some sectors. Wasn’t this scenario conducive to lower spending, and hence lower inflation, in the non-tradables sectors?

Rajan asks a rhetorical question: “How could the Reserve Bank have brought down inflation without killing demand? By bringing down the public’s expectations of inflation and by not giving in to the clamour to slash interest rates!”

He is right on this, and managing inflationary expectations is where he can take full credit. Specifically, the message went down very well with the UPA government in its final years, as the government finally got down to the job of cutting the fiscal deficit. However, the real fall in inflation had many contributing causes, including the sharp rural and industrial slowdown and the drop in investment by both the private and public sectors.

Rajan was, and still is, a good Governor. He did the right things to send a message to both policy-makers and citizens that inflation is too high, and that banks were going broke.

But this should not lead to claims that monetary policy directly contributed to reducing inflation. What monetary policy does is send signals on what is wrong, and what needs fixing. That is where Rajan should claim credit. The trajectory of inflation depends on many factors and the impact of monetary policy alone is difficult to calculate.

Rajan has done the right things, and that is what he should be evaluated on.

Jagannathan is former Editorial Director, Swarajya. He tweets at @TheJaggi.

Get Swarajya in your inbox.

Magazine