World

Weaponisation Of The Dollar And The End Of Its Role As The Global Reserve Currency

Mohal Joshi

Apr 12, 2022, 01:38 PM | Updated 01:37 PM IST

Save & read from anywhere!

Bookmark stories for easy access on any device or the Swarajya app.

Today most of the world’s trade is conducted in US dollars (USD). This is the “defacto” global reserve currency for trading between most nations.

Bretton Woods And Petrodollar System History

Around the end of World War 2 (WW2) the “Bretton Woods” system was setup by a group of 44 nations in a conference held at Bretton Woods, New Hampshire (USA).

This monetary system established the rules for commercial and financial relations among the participant nations which included United States, European nations, Australia and many others. Member nations would peg their currencies to the US dollar, and the US would peg the US dollar to gold, at a price of $35 an ounce.

The central role of the dollar in world trade eventually forced the US to run a persistent trade deficit. By the early 1960s, the US dollar's fixed value against gold (35$ per ounce) was seen as overvalued. The profligate spending due to the Vietnam war and the welfare programs during the 1960’s meant that the dollar was seen as being overvalued against its gold reserves. A few countries tried to withdraw the gold that they had sent to the United States for safekeeping.

After a run on its gold reserves, in August 1971, then-President Nixon declared a temporary suspension of the dollar’s convertibility into gold and thus the original Bretton Woods system collapsed. By 1973, the Bretton Woods system was replaced by freely floating fiat currencies. The dollar subsequently lost 20 per cent of its value (devalued against gold).

Unconditional support by the United States for Israel during the 1973 Yom Kippur war angered the Middle Eastern Arab states. These oil producing OPEC states placed an oil embargo on the United States. As a result of this, the price of oil quadrupled, causing a severe economic shock for US and other oil importing nations. This added to the stagflation of the 1970’s increasing economic misery in United States. To better relations with Saudis and bring down oil prices, President Nixon in July 1974 sent his Treasury Secretary William Simon on a secret mission to negotiate a deal with the Saudis.

As per the agreement US would buy oil from Saudi Arabia and provide the kingdom with military aid/hardware. In return, the Saudis would use their oil wealth (which had gone up a lot especially given the price rise) to buy US Treasuries (i.e.US debt). This mechanism (of pricing oil in just US dollars) was soon adopted by other OPEC countries. This once again confirmed the hegemony of the US dollar as the mechanism for global trade (for e.g., oil purchases in the British pound fell from 20 per cent to 6 per cent in just a couple of years post this event).

This was referred as to the “Petrodollar” system, where oil was exclusively priced in US dollars and the oil producing nations, in return, ploughed their oil revenue money back in the United States. The purchase of US Treasuries with the oil revenue helped to keep the US dollar strong and the US debt cheap.

The US government, due to these foreign purchases of US debt, was able to keep borrowing costs lower and was unencumbered to generate even more larger sums of debt which it used to finance wars, social welfare programs etc., over the next few decades. For the OPEC nations, it allowed them to park their excess money in US Treasuries which was considered as one of the safest investment products around given the long-term stability of the dollar system and the US government creditworthiness (i.e., implicit understanding of not defaulting on their debt obligations).

Russian Sanctions And Its Implications

Russia’s invasion of Ukraine in February 2022 resulted in the Western nations (including USA and Europe) employing some of the toughest sanctions to date, some of which were previously only employed against pariah nations like North Korea, Venezuela, Iran etc. Russia was removed from the SWIFT banking system (a messaging system that is used to faster and quicker cross border trade/payments between trade partners). Various banks and financial institutions have ceased operations inside Russia and also refuse to do any transactions with entities inside Russia.

However, in an unprecedented move, US led a move to freeze Russian Central Bank forex assets. As per reports around half of Russia’s $600 billion worth of the forex reserves which were outside Russia have now been frozen.

Traditionally in the Petrodollar system many Central Banks also parked their Forex reserves and gold with US and other Western nations for safekeeping. Many preferred to keep their assets overseas in the West to prevent it from falling into the wrong hands due to corruption or local unrest and also keep it in safer US Treasuries which are less affected due to the vagaries of fluctuating local currencies.

Now in the space of a year both the Afghan and Russian forex reserves overseas have been frozen with a proverbial “single click of a button”. Already a portion of the $7 billion of the Afghan reserves is going to be split among the 9/11 families and humanitarian assistance. So, in Afghanistan’s case, even if relations normalise with the ruling Taliban elite or even if they are overthrown by a friendly democratic regime, some of the money will never come back as it is already being given away.

Something similar where the frozen Russian central bank reserves are given to the Ukrainians would not be too farfetched at this point. Keeping aside the moral question of the money helping the Russians and the Taliban, this has opened a Pandora’s box on whether the money in US Treasuries and dollars especially parked overseas, is safe or not.

Even the Wall Street Journal in its recent op-ed opined with the headline “If Russian Currency Reserves Aren’t Really Money, the World Is in for a Shock”. The unwritten principle from the past few decades that central bank reserves are sacrosanct has been thrown out of the window in a flash.

Any country that threatens the West/US alliance or dares to cross them could have itself on the wrong end of sanctions including being pushed out of the dollar based global monetary order. Nations which have gradually earned their forex reserves with years of traded surpluses will be wary of putting their wealth at the mercy of other powers.

The Russian ruble, after getting devalued a lot versus the US dollar, has now somewhat stabilised but it is still ~40+ per cent lower vs before the Ukraine invasion. With Russia being frozen from the Western banking system, it will be hard to get dollars to transact with rest of the world. Russian central bank to stabilise their local currency (ruble) prevented citizens from exchanging rubles for dollars.

Russia, even before 2022, had been gradually increasing its trade with China in yuan/rubles (i.e., moving away from the dollar). Russia, on a daily basis, exports around $1 billion of natural gas to the rest of Europe. They are now asking the European gas importers to pay in rubles instead of dollars. This forces European nations to now exchange their dollars and euros for rubles to fulfil their energy payments to Russia. This creates more demand for rubles helping stabilise their currency against the dollar/euro.

India has also been using the rupee-ruble pair to avoid CAATSA sanctions. Now, with Russia being cut out of the financial system, this trade is bound to grow, given India’s dependence on Russian military hardware/spares.

If more nations to de-risk themselves from ending up in a position like Russia start moving away from the dollar system, it chips away at dollar hegemony in the long run. Already OPEC nations such as Saudi Arabia have sought to explore deals to sell oil to China in yuan (vs dollars).

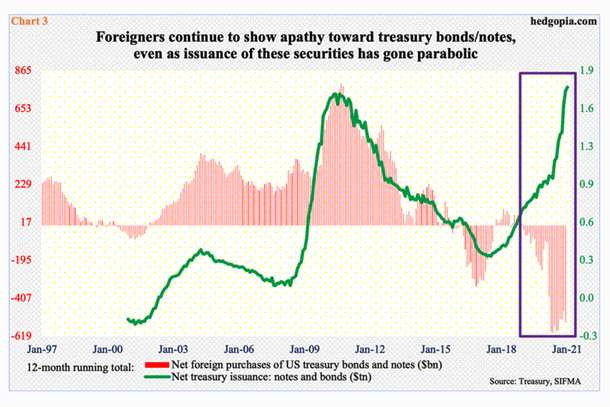

Since the past 7+ years, foreigners have been net sellers of US Treasuries (vs being net buyers pre 2015).

Now, if other nations start to more aggressively sell US Treasuries (on a net basis) than ever before, this will increase the cost of borrowing for the US government, which is already facing high levels of debt. To keep interest rates low, the Federal Reserve would have to step in as a measure of last resort for buying these Treasuries. Otherwise, with very high interest rates, it risks bringing down the whole highly leveraged and indebted financial system.

China, given its huge US Treasuries portfolio (in excess of $1 trillion reportedly), if it has plans for re-unification with Taiwan, will want to sell these Treasuries before making any move on Taiwan. Any country by itself selling US Treasuries might not have massive impact, but if significant number of countries follow through, there would be long term issues for the dollar and the United States.

Many smaller countries who have dollar denominated debt can’t print out of a crisis like how the US does. Being the reserve currency, the US can print more of its own currency, which, combined with the foreign buyers of US Treasuries, allows US to print its way out of any financial crisis. However, the cost of all this printing of US dollars comes with bad consequences for other nations who now are mired even deeper into financial repression.

Alternatives To The Dollar: Gold And Bitcoin?

In 1944 during the Bretton Woods conference, British economist John Maynard Keynes proposed BANCOR, a new neutral reserve currency that would be used for settling international accounts. However, the US overruled this proposal in favour of a system of fixed exchange rates using the US dollar (which was a gold standard currency for central banks) as a reserve currency.

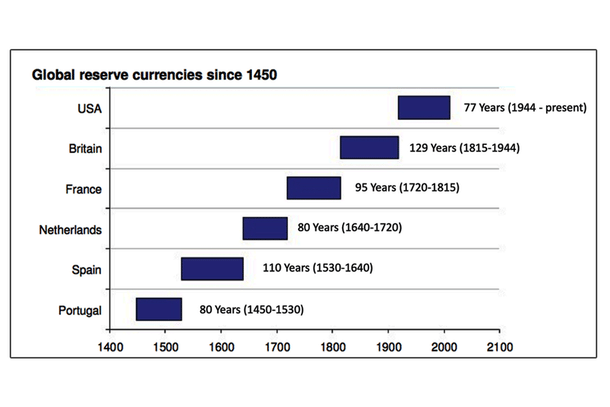

Now, if commodity rich nations such as Saudi Arabia and Russia suddenly decide to not use the dollar for global trade, then the trillion-dollar question is, what would be the next global reserve currency? Looking back at the history of over the past few centuries, one has seen that the global reserve currency has changed hands every ~80-100 years. The dollar is nearing the 80-year mark also so a change of the guard in the next few years would not mean a deviation from the historical norm.

The global reserve currency has been closely aligned with the overarching power in the world at that moment in history. China being a rising power, sees itself as a Great Power (in its own mind at least) would be in the mind of many as “calling the shots” in what the next global currency would be.

While, in theory, China would not mind having most of the world trade be conducted in yuan but given the Triffin dilemma that US faces today, this would be an obstacle. The Triffin dilemma is the conflict of economic interests that arises between short-term domestic and long-term international objectives for countries whose currencies serve as global reserve currencies.

The use of US dollar for global trade creates a big demand for dollars from all around the world leading to the dollar strengthening relative to other global currencies. This dollar strength made US exports become uncompetitive compared to its peers overseas. This has led to the hollowing out of the US manufacturing sector and a flight of jobs over the past few decades. This has imposed high costs on those who worked in blue collar jobs across many areas of US including the so-called “Rust Belt”.

China being an export led economy, would not want to fall into the same trap as United States. While they would like to have global trade denominated in yuan in principle (as a matter of national pride), one doubts if they want their exports (which is a big part of their economy) becoming more expensive. Also, for all trades to settle in yuan, China would have to export yuan to many other nations who would need yuan to settle trade with their trading partners. Given the strict capital controls in China, it would be surprising if China allowed a lot of yuan to go out of the country to foreign shores.

China has benefitted from the dollar system (running up trade surpluses year after year) where they can have their exports cheaper due to dollar strength so they would not mind having the reserve currency as something other than their own currency.

Even if China wanted to setup yuan as a default reserve currency, the question is that, would other states fully embrace it? Today due to tensions with the West, Russia is forced into a friendship with China but they were not on the best of terms always including a military skirmish in 1969. Chinese from time to time bring up their territorial claims in Russian Far East including Vladivostok, which they say were given up by China as part of unequal treaties during their “150 years of humiliation” with foreign powers, and now they want it back.

Many other Asian neighbours including India, Vietnam, South Korea, Japan etc., with which China has adversarial relations, would also be wary of adopting a yuan-based reserve currency where they would be dependent on China to obtain yuan for their trading. Also, in the event of military hostilities with China or its allies (like what Russia is facing right now), they could be “cut-off” from the reserve currency yuan which would be determinantal to them.

A return to a system like BANCOR (neutral reserve currency) proposed by Keynes in 1944 would require active cooperation between many nations across the world. With active geopolitical tensions among the various set of nation pairs: Russia and USA, USA and China, Europe and Russia, Saudi Arabia/UAE and Iran etc., the chances of another “Bretton Woods” kind of consensus are next to nil.

Many macroeconomics watchers Luke Gromen macro analyst and founder and president of Forest for the Trees (FFTT), have mentioned that in future, a world where neutral assets like Gold or even Bitcoin might be used to settle transactions for cross border trade. Gold and Bitcoin being neutral assets removes the Triffin dilemmas for nations while also providing options which are also, to an extent, free of counterparty risk.

GOLD: It has been around for centuries and was used as medium of exchange in older times. Gold reserves can be kept locally, which eliminates depending on other nations to purchase, let’s say, dollars or yuan or some other currency to affect trade. Russia already is reportedly considering accepting payment for natural gas from “unfriendly nations” in gold. This eliminates the need to convert the dollars into rubles they get for oil/gas payments which is now harder given the sanctions.

Russia has one of the highest gold reserves in the world at $130 billion+ which they can use as collateral to trade (in lieu of now hard to come dollars). Greater adoption of gold backed trading is bound to increase the price of gold, in which case, given their large reserves, it is going to benefit them the most. Nations could directly trade with each other in gold, eliminating the threat of sanctions via third parties.

However, transporting huge amounts of gold between nations would have its unique challenges in terms of transportation, security and insurance for such transfers. Gold also requires strenuous audit for its weight, quality/purity which would be other overheads added in this kind of monetary system. One can, in theory, settle the trade between two nations on a “net basis” (vs trying to pay by gold for every small transaction between both), but this would entail the government having to pay the individual entities till the overall trade is settled as one final transaction.

BITCOIN: The other possibility for the next global reserve currency floated by some (especially by Bitcoin enthusiasts) is Bitcoin. Unlike gold which is physically hard to move given its weight and the cost of security/transportation, Bitcoin has no such challenges.

The amount of Bitcoin on the open ledger can easily be verified, and there is no counterparty risk if it is held securely by individuals/nations. Also, gold requires large scale auditing of gold and verification of the gold itself (i.e., purity), which Bitcoin does not.

Russia recently has indicated its willingness to even accept Bitcoin for its oil and gas. Accepting Bitcoin for all global trade right now would be a Bitcoin purist’s ultimate dream, but given the amount of liquidity in the Bitcoin market, it would be interesting to see how such a thing would play out. More development in the L2 (Layer 2) application space like Lightning Network could help overcome this challenge.

While with the passage of time, the volatility in Bitcoin is reducing (on a relative basis) but for some traders, the volatility might be unappealing to transact in. A mitigation mechanism like instantly converting the Bitcoin transactions back into local fiat currencies would help overcome the volatility issue. Bitcoin, either on the main chain or via L2 applications like Lightning Network, with its low fees, would be cheaper in terms of costs to move money from buyer to seller compared to traditional finance channels.

An example of this is the Lightning network used by El Salvadorian expatriates sending money to relatives back home via the Lightning network vs traditional methods such as Western Union. The money is sent back home at a fraction of the cost compared to Western Union, plus there is no need for their family members to make an arduous trek to the nearest Western Union office, which could not only be time consuming but also prone to interdiction by criminal gangs who could ask for their “cut” in lieu of safe passage.

Bitcoin network being decentralised, it would be exceedingly hard for nation states to block other nations from trading in it making it highly censorship and sanction resistant. A nation does not have to remain in fear that antagonising Nation A, where it parks its forex reserves or angering Nation B, which has the global reserve currency, can inflict economic pain if it does not do the bidding of the other nation. With Bitcoin, no government or a set of actors can inflate the currency away or manipulate it to the detriment of other nations.

The recent events have brought into focus the pitfalls of a reserve currency where other nations can’t control their own reserves and hence their own economic destiny. Once friendly nations could, in the future, turn on one another leading to sanctions on the smaller nation and/or it being cut off from the global economic system. A bigger nation could use the threat of sanctions to “mold the behavior” of a smaller state to its own liking.

This has brought into focus neutral assets that are harder to sanction, block and seize, such as Gold and Bitcoin. Once derided as flights of fantasy of “gold bugs” and “bitcoin maxis”, a transition to them being used to settle cross border payments does not seem as outlandish as just a few months ago.

Russia and even other states might opt out of the current system by in the future explicitly denominating a barrel of oil in ounces of gold or a cubic foot of natural gas in Satoshi’s (i.e., smaller unit of Bitcoin). Given the current commodity price spikes, many nations (unless they diversify quickly to other sources which takes some time and cost) might be forced to pay Russia by these new mechanisms due to the lack of choices. [i.e. forced to the new payment system “kicking and screaming” vs gradually adopting it voluntarily]

This does not mean that the US dollar will lose its reserve assets tomorrow, but it is on the way out. Like on the geopolitical front, as the world moves from a unipolar American to a multipolar world, there could be something similar in the economic sphere where we could have multiple reserve currencies operating at the same time! Legendary investor and billionaire Stanley Druckenmiller, in an interview last summer, said that he does not expect dollar to be the reserve asset within 15 years.

The 2020’s decade has been one of massive upheaval with all sorts of problems: pandemic, supply chain issues, massive central bank printing, inflation, geopolitical tensions, great power rivalry, war, commodity price shocks etc. Given the events of the past couple of years in this decade, it would be hard to say what the future holds in terms of the next reserve currency, be it Gold or Bitcoin or something else, but it would not be surprising that the if the dollar does not have global reserve currency status by the end of this decade.

This article was originally published on Crowd Wisdom on February 15th, 2022.

Also Read: NATO Is Past Sell-By Date: Self-Serving Uncle Sam Is No Longer Europe's Best Guarantor

Get Swarajya in your inbox.

Magazine